This is part 2 of a series on what we really know about growth in developing countries, where I establish a common ground for EAs to think about specific interventions that could increase growth. In this series, I lay out some stylized facts about developing countries from different angles, drawing on modern "macro-development" research that aims to credibly estimate the causes and constraints of growth and development. Part 1 focused on the sectoral transformation as countries move away from agriculture; part 2 takes a much more granular approach, and focuses on the growth of firms.

Firm dynamics in developing countries

In part 1, I stated without justification that agricultural transformation was necessary for economic growth. It's practically doctrine for development economists! But people pushed back in the comments, because I hadn't made an argument to justify it. This time, I want to motivate my angle clearly, because I personally believe firm dynamics is the most important angle from which to conceive of growth interventions, and I want to convey why.

The founding question of growth/development economics is "how do we make poor countries grow?" This is a powerful motivating question, but it was too abstract: the result was a lot of cross-country empirics which don't have much insight for us today. We can make some progress by breaking countries down into sectors, which was the focus of part 1. But we can go even further by recognizing the obvious truth that a country's output is the sum of its firms' outputs. When you recognize that, you can reframe the founding question of as "how do we make firms in poor countries grow?" There are three mechanical answers: you can make new firms enter, you can make each firm grow, and you can make low-growth firms exit. These phenomena are what I will refer to together as firm dynamics, though I don't think the entry of new firms is important[1], so I will focus only on within-firm growth and between-firm reallocation.

What makes firm dynamics special to me is that it feels like the closest thing we have to a sufficient condition for growth. The development process is full of necessary conditions. If Tolstoy had been a development economist, he might have said that every rich country is alike, but every poor country is poor in its own way. Failing to industrialize, bad institutions, poor geography—these are all factors that can hold back growth. But it is almost a mathematical truism that if a country's firms are growing on average, and low-growth firms are exiting the market, then that country will grow. And while "how do we make countries grow?" produces platitudes, "how do we make firms grow?" has real answers. Obviously, making firms grow is not easy—but it definitely seems easier than all other plans of attack.

I'm going to frame this discussion in terms of the manufacturing sector; partly because most of the studies about manufacturing firms, and partly because I think manufacturing productivity growth is really important for overall growth, and I want to use firm dynamics as a lens on how to increase growth in manufacturing. But I suspect these facts are true for firms in the agriculture and service sectors as well. (Farms are just a kind of firm!)

Caveat lector: this is not a comprehensive summary of what matters for firm growth. Many readers will never forgive me for excluding one particular idea[2] and I don't cover many important topics (e.g. credit constraints, hiring constraints, weak contract enforcement); I made a judgment call on which topics were more important, and you should know that this is only the tip of the iceberg.

1. Firms in developing countries are smaller, more informal, and more stagnant than in rich countries.

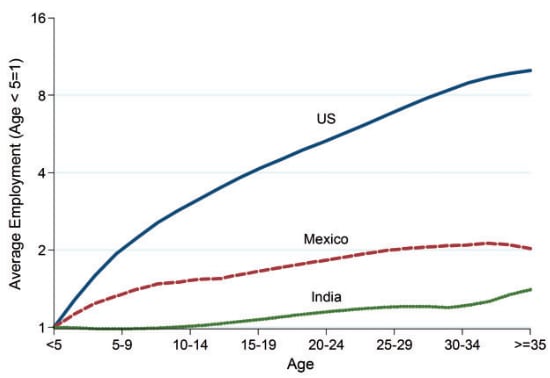

Here is the figure that radicalized me on firm dynamics: (Hsieh and Klenow, 2014)

In the US, firms either grow or die; if a firm survives to age 10, its employment has on average tripled from when it started. Of course, most firms don't survive to age 10, since overall employment growth is much smaller than that tripling. The growing firms are gaining employees from all the firms that exit the market, which is why exit is as important to this figure as growth. In contrast, firms in India are completely stagnant. Mexico is somewhere in between, but closer to India. Subsequent research with other developing countries has placed them in between the India and Mexico lines, all far below the US. Firms just don't grow in developing countries, even when the country itself is growing. This stagnance also explains why firms in developing countries are overwhelmingly small (97% of firms in Mexico, Indonesia and India have less than 10 employees); if you started with a collection of small firms and had the same "grow-or-die" pressures present in the US, you would quickly end up with a smaller number of large firms—which is a characteristic of rich countries.

Instead, growth seems to take the form of new firms entering the market, and staying small. Can that be a viable growth strategy? Probably not. First, many goods can't be produced without scale. (Imagine a 5-person steel mill.) Second, modern technologies involve high fixed costs and lower unit costs, making them only feasible with a certain scale of production. Third, a certain size is needed to have specialization within the firm; Bassi et al (2023) find that manufacturing firms in Uganda have very little specialization, which reduces their productivity significantly. So we do need firms to grow in productivity, and to take market share and employment from low-growth firms.

An important dimension to this graph is the informal sector. Informal firms, small and unregistered firms which operate outside of formal regulations, make up the vast majority of firms in developing countries, and employ the majority of workers. How should we think about the informal sector?

Some people argue that informal firms are suppressed entrepreneurs, who are extremely productive but are held back by government regulations and lack of property rights/loans. (de Soto 2000) However, there's no evidence that informal firms ever actually grow into large formal firms, and informal firm operators look very different from formal firm operators in many ways (e.g. they are less educated). Others argue that informal firms are unproductive parasites who dodge regulations and prevent growth by more productive formal firms. (McKinsey 2004) However, when surveyed, formal firm managers don't view competition from informal firms as a serious problem (Schleifer and La Porta 2008). The simplest explanation for these patterns is that informal firms are not actually firms per se, but rather a social safety net of last resort for poor people who cannot find stable jobs. As countries grow, self-employment shrinks and the formal sector expands 1-1, suggesting that the former owner-operators of informal firms move to being workers in formal firms. Therefore, it makes sense that informal firms are stagnant; they are not "businesses", but rather a symptom of the lack of good jobs.

Thus, it's likely that the informal sector is a key cause of stagnant firms in the graph above. Unfortunately, Hsieh and Klenow don't create an analogous graph for the formal sector alone, so it's hard to know exactly how much of the lack of firm growth can be explained by informality. But if the informal sector is really a social safety net, then if firms in the formal sector become more productive and hire more workers, the informal sector should melt away. Thus, formal sector firm growth will be key to making developing-country economies more dynamic.

2. Small market size and information frictions constrain firm growth.

Firms are limited by the market they can reach. In developing countries, urban mobility is very low (Akbar et al, 2023) and so people are more likely to buy from firms near them, regardless of quality. When gas prices increased in Mexico City, it caused a proliferation of low-quality retail stores which only survived because people would not commute to higher-quality stores further away. (Ramos-Menchelli and Sverdlin-Lisker 2022) Moreover, developing countries have high internal costs of transporting goods (Atkin and Donaldson 2015), both because of high physical costs and high markups in the transportation sector (Allen et al, 2022). Thus, firms face barriers to selling to large markets; if they are not in big cities, it's expensive to transport their goods to the big cities, and even if they are in big cities, consumers will only go to the closest firms.

A more subtle point is that firms can also sell to at most the number of people who are aware of them, and if consumers are only aware of the firms closest to them, then they will never switch to purchasing from more productive firms. Jensen and Miller (2018) look at boat-builders in India and find substantial quality dispersion, driven by fishermen mostly purchasing from the boat-builder in their village, regardless of quality. But after the spread of mobile phones, fishermen travelled more to other villages to sell their catch, and encountered more boat-builders; the result was that the most productive boat-builders grew while the unproductive ones exited; the number of boat-builders fell by 60%, while firm size increased dramatically among the surviving firms. Thus, information spread led the most productive firms to expand and increased firm growth.

The direct effect of these two frictions is obvious: firms sell less, so they grow less. But their indirect consequences are possibly even more important: without prospects to sell to a large market, firms don't have any incentive to invest in productivity improvements. In an RCT, Ugandan maize farmers did not invest in increasing the quality of their produce, unless they were given the opportunity to sell to larger markets. (Bold et al, 2022) Investing in higher productivity will not actually increase your profit if you sell to a small market, so firms won't do so, even if they can. These frictions also defang market pressures from pushing firms to improve their productivity, by making firms monopolists in their tiny corner of the economy. In the next two sections, I talk about ways to help firms learn and adopt better technologies/practices, but those will be useless if firms don't have an incentive to learn or adopt better technologies/practices. Thus, fragmented markets are possibly the biggest barrier to firm growth.

Physical market size has a clear solution: better transportation infrastructure. When India built large-scale transportation infrastructure across states, it increased competition and boosted the market share of productive firms. (Asturias, Garcia and Ramos 2019) Better transportation infrastructure also induces competition in the transportation sector and thus reduces markups, making it easier for good firms to "export" to other areas of a country. E-commerce logistical chains can also increase market access for firms; e-commerce expansion in China increased the exporting of goods from cities to the countryside (Couture et al, 2020), which could have beneficial market size effects for urban manufacturers. Information frictions are a bit more fuzzy, but Jensen and Miller's results suggest that mobile phones and internet access can reduce them.

3. Firms in developing countries do not use advanced technologies or management practices.

Firms in developing countries lag behind the frontier of technology (Cirera, Comin and Cruz 2022); they use less advanced technology than firms in rich countries within the same area. Some of this is explained by differences in firm size (small firms will naturally not benefit as much from high-fixed-cost technologies), but even large firms in developing countries use frontier technology at a much lower rate. One explanation that the authors highlight is a quasi-Dunning-Kruger effect among firms; technologically unsophisticated firms tend to rate themselves as much more advanced than they are. This behavioral bias could explain why firms upgrade their technology less than optimally.

One simple way to address this gap with the frontier might be to import advanced technology from rich countries, that they can use to produce more efficiently. This can work; Bai et al (2022) show that when Chinese automakers enter joint ventures with Western automakers, the quality of their cars improves. However, a key condition is that firms get knowledge along with machines. Giorcelli and Li (2023) look at a Sino-Soviet partnership during the Cold War, where the Soviet Union supported the construction of over a hundred industrial clusters in China. These plants would get machines from the Soviet Union, as well as training of Chinese workers by Soviet engineers on how to operate these machines. The Sino-Soviet split abruptly ended this arrangement before it was complete, leaving a neat natural experiment: some plants had received machines and training from the Soviets, others had received machines without the subsequent training, and still others had not yet received anything at all. The plants which received advanced machinery were more productive than the plants which received nothing, but the effect died out within 20 years (the replacement period for the machines). However, the plants which received advanced machinery and engineering training on how to use them stayed more productive for decades, and even exported more after China's globalization. Thus, successful technology transfer requires knowledge transfer.

This condition also demands a certain level of skill from a country's workforce; e.g. if a country has a severe shortage of good engineers, then it may not be possible for firms to use advanced machines, because they don't have good engineers who can absorb that knowledge. Moreover, leapfrogging (where firms go from primitive technology to advanced technology) doesn't seem to work. When firms upgrade their technology, they move incrementally up in complexity rather than leaping to the frontier (Comin, Cirera and Cruz 2023) suggesting constraints to absorbing technology that is too advanced. So importing technologies that are somewhat more advanced, and training workers to use them, can improve a firm's productivity.

In addition to technologies, firms in developing countries have weak management practices. In an RCT with Indian textile firms, Bloom et al (2013) found that management training from a global consultancy reduced wastage of materials, increased labor productivity, and improved the quality of outputs. Rough calculations suggest that the increased profitability would have been more than the consulting fee, even if the firms paid full price (they paid nothing as part of the RCT). This is surprising, given that most of the firms in their experiment had been in business for 20+ years, the management practices they learned were no secret, and they had ample benefits from improving their practices. So it's not clear why they were leaving money on the table. Nonetheless, it seems to be true that firms in developing countries are not well-managed, and this management gap matters. Analogous to frontier technology, there is a lot of promise in importing management practices as an intervention. This RCT provides the strongest evidence for this possibility, and a straightforward template. Giorcelli (2019) also finds that Italian firms who participated in an 8-week management training program in the US became much more productive than other firms who lost out on the program because of a budget cut, and the effect persisted for decades. So it seems quite likely that training firms in developing countries on management practices is an effective intervention, but exactly how to best operationalize that idea is still an open question.

4. Interaction with the global market helps firms learn frontier techniques and become more productive.

One insight from the East Asian growth miracles is that interacting with the global market (e.g. through exporting, or transacting with multinational firms) can be critical to improving firm productivity. The main reason for this is that it helps firms learn from global firms who have frontier technologies and practices, and thus increase their own productivity.

Bustos (2011) finds that when Argentina and Brazil liberalized bilateral trade, firms in Argentina that gained more export opportunities increased their spending on technology, suggesting that access to foreign markets incentivized firms to upgrade their technology - this is especially important given that firms in developing countries use less advanced technology. Atkin, Khandelwal and Osman (2017) randomized export opportunities to rug manufacturers in Egypt, and found that treated firms became more profitable—in an important way. Counter to what you might expect, the exporting firms did not produce any faster or cheaper than the control firms—but their rugs were significantly higher quality than the rugs made by the control firms. When the researchers asked them to make rugs of a standard quality, they did so faster than control firms—showing that they could choose to produce normal rugs faster, but they chose to translate their productivity gains into quality rather than cost.

This distinction matters; quality upgrading is the holy grail of firm productivity growth, while cost reductions are an acceptable alternative. Why? Because in most manufacturing sectors, reductions in cost are fundamentally limited, but there's no limit on how high-quality you can make a product. After all, Apple didn't become a trillion-dollar company by making phones and computers cheaper than every other company. Moreover, having a higher-quality product differentiates you from all the other producers, and makes you hard to replace; many companies can make great phones, but only one can make the iPhone. In contrast, when a country's firms specialize in low-cost manufacturing, they can always be displaced by firms in another low-income country whose labor costs are low enough to compete. This is why even though China began as a low-cost manufacturing destination and "made in China" used to be a negative statement, the Chinese government invested in moving up the value chain and producing higher-quality goods. Quality upgrading is everything! So the fact that exporting increases firms' quality is very important, and suggests that creating export opportunities is one of the most effective ways to increase firm productivity in developing countries.

Another way to interact with the global market is through foreign direct investment (FDI). Countries pay large amounts of money to attract multinational companies (MNCs), partly in the hope that interacting with MNCs will have knowledge spillovers to domestic firms. Alfaro-Urena, Manelici and Vasquez (2021) show that when multinationals enter Costa Rica, their suppliers become significantly more productive than similar non-suppliers. Importantly, this isn't just because of scale economies; selling to the government (with similar order sizes) has no comparable effect on firm productivity. the researchers also compare the effect of selling to a MNC with selling to the government, and find that selling to the government has no effect on firm productivity, while selling to an MNC does. So what makes the MNC special? The likely explanation is that MNCs bring knowledge and tell their suppliers how to be more productive (e.g. by having expectations of quality that force the supplier to adopt good management practices). Thus, FDI has important spillovers that can increase the productivity of domestic firms.

Addendum: industrial policy

Incredibly, I've gone through a whole essay about manufacturing firm growth without mentioning industrial policy. Industrial policy is broadly defined as state intervention to change the long-run composition of economic activity between sectors. Most commonly, governments use it to increase the size of the manufacturing sector, or particular kinds of high-value manufacturing. Given the importance of manufacturing for growth historically, and the success of industrial policy case studies like Korea, industrial policy is perennially on the minds of developing-country policymakers.

Even though industrial policy is defined as promoting the growth of sectors, when the rubber meets the road, industrial policy is implemented at the level of firms. Today, most industrial policies are granular, often targeted at individual firms, and usually consist of subsidies and export promotion (Juhasz et al 2023). It follows that the key to a successful industrial policy will be that it successfully catalyzes firm growth. That means we already have a few lessons for how governments can implement effective industrial policy:

- Industrial policy should focus on overcoming growth barriers, not entry barriers. We already saw that firms in developing countries face constraints on growth, rather than on entry. Accordingly, in a study of the global shipbuilding industry, Kalouptsidi, Barwick and Zahur (2023) find that in China's industrial policy, production and investment subsidies were effective at growing China's share of the world market, while entry subsidies were ineffective.

- Industrial policy should focus on increasing the market that firms in a sector can sell to. The most obvious and successful way this can happen is through export promotion, which has the additional benefit of increasing firms' learning from the global market.

- Industrial policy should encourage domestic firms to adopt advanced technologies. When Korea industrialized, subsidies for foreign technology adoption increased the amount of technology transfer from Western firms to Korean firms, and boosted the long-run size of the manufacturing sector. (Choi and Shim 2023)

In general, successful industrial policy will be tightly targeted at overcoming barriers to firm growth in a sector.

Conclusion

Firms in developing countries are smaller, more informal, and more stagnant than in rich countries; this is a problem because in my view, more creative destruction is a key condition for growth. The main barrier to firm growth, and the culling of low-productivity firms, seems to be small market size (both because of physical frictions and information frictions), and increasing market size is crucial to incentivize firms to be more productive. There are many ways to increase firm productivity, but the two that stand out are importing management practices/technology from the frontier, and having domestic firms interact with the global market through exporting and FDI. These facts also provide insight into how developing countries can effectively implement industrial policy.

First, developing countries have much higher self-employment rates than developed countries, suggesting that they have much more firm entry than rich countries. Second, Peters (2020) compares Indonesia and the US, and finds that barriers to firm entry are similar between Indonesia and the US, but the barriers to firm expansion are much higher in Indonesia. So I don't think it's likely that any interventions that increase the entry of firms will be helpful for growth. Finally, the Hsieh and Klenow graph in section 1 suggests that growth currently mostly takes the form of entry, while within-firm growth and between-firm reallocation is where developing countries really lag developed countries. ↩︎

Probably the single biggest concept of macro-development in the 21st century is misallocation, which intuitively corresponds to the idea that more productive firms have lower market share in poor countries than they do in rich countries. In other words, not only are firms constrained on average, but the most productive firms are more constrained than the least productive firms. This insight gives rise to a lot of interventions or policies that are designed to alleviate the constraints of the most productive firms - e.g. size-dependent regulations effectively tax large firms more than small firms, which is bad because large firms are more productive, so eliminating size-dependent regulation could increase productivity by allowing large firms to expand and take market share from small firms. Misallocation is an important insight, but I don't feel confident that misallocation is quantitatively important in explaining cross-country productivity differences, for methodological reasons (it's hard to distinguish between measurement error and misallocation, and most ways of estimating misallocation treat all firm heterogeneity as misallocation). ↩︎

Nice post, Karthik! Nitpick, you may want to spell out the meaning of the acronyms MNC (multi-national corporation) and FDI (foreign direct investment) in their 1st instances.

Done, thanks!

Executive summary: Firm dynamics are critical for economic growth in developing countries. Small, informal, and stagnant firms characterize poor countries, while market pressures ensure firm growth or exit in rich countries. Increasing market size and exposure to global markets can incentivize developing country firms to adopt better technologies and management practices.

Key points:

This comment was auto-generated by the EA Forum Team. Feel free to point out issues with this summary by replying to the comment, and contact us if you have feedback.

Thank you so much for this valuable breakdown of interventions, Karthik.

I am an absolute layman but in an effort to respond to your call from an entrepreneurial eye, I tried to dig further into the management training intervention mentioned in the Bloom (2013) paper. While the impact of this intervention is meaningful if not impressive, as you have noted, it is unclear how to operationalize this at scale.

However, something I found interesting was that one of the main barriers for firms not already investing in these practices is informational. Specifically, their owners didn't know their relative quality compared to their peers. Given this, I was wondering if it might be possible to have a OPower-like intervention which could provide information about their relative performance to their peer firms to motivate them to perform better. This seems especially plausible since the authors mentioned that the ROI of the training was about 130% in the first year and at least these large firms in the study didn't have financial barriers.

However, it is not clear to me what incentives the firms might have to share their quality information or if there are external sources for us to gather this information.

I'm ambivalent about whether the barriers really are informational. When firms are surveyed, they claim to be much more advanced than they are, but my suspicion is that this is just a cope. They want to tell these World Bank surveyors that they are cool and advanced firms even if they know they are not. But it seems worth trying for sure.

In the Bloom study, they mention that information spillovers across firms are very limited, because owners guarded this information. But there were still local spillovers (to firms in the same town), possibly because of communication between workers at different firms.