TL;DR:

The "mean" cost-effectiveness of interventions with uncertain impact can be misleading, sometimes significantly.

We want to consider , not .

2023 Edit: I now think that the top comment is right: we want to use , I'll keep the rest of the post as is, as I still think it can be useful

Epistemic status (how much I'm sure of this): I'm pretty confident about the main claim, but still confused about the details, I end the post with some questions.

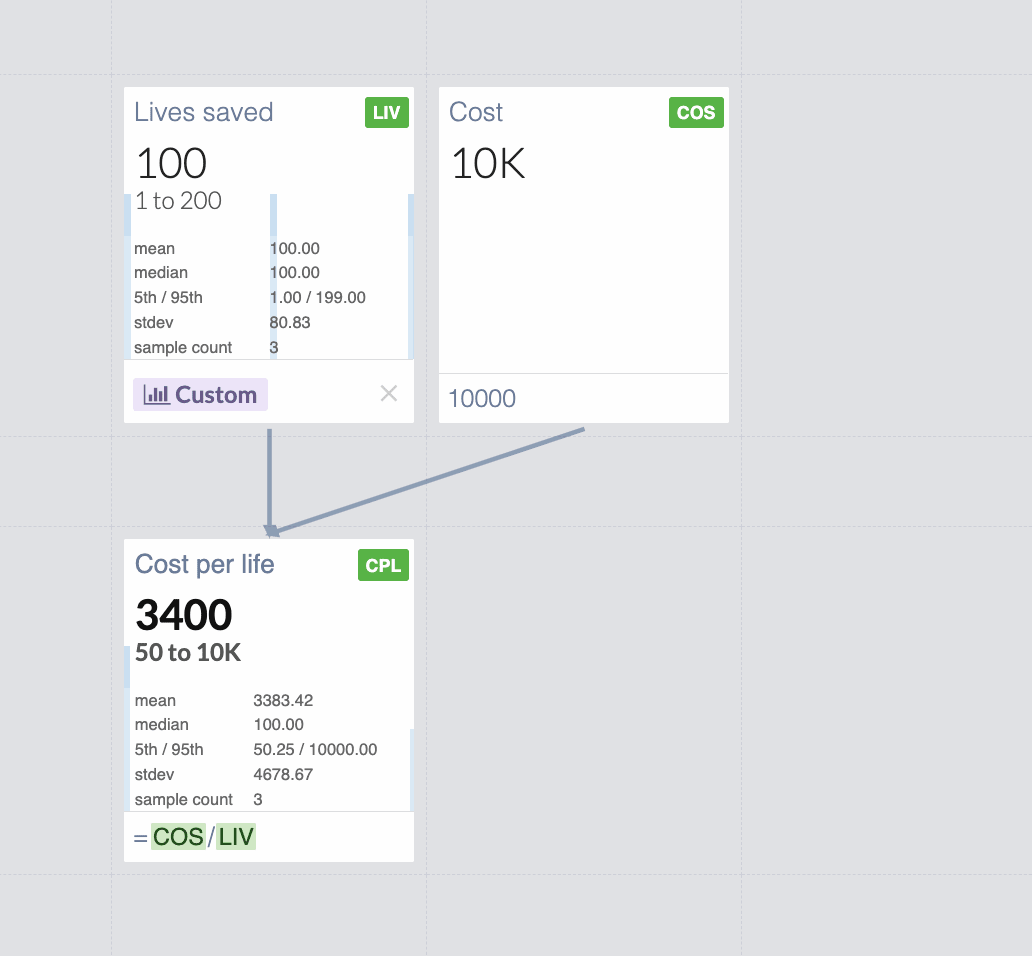

Minimal extreme example:

Let's say that you have a magical intervention that has:

- 33% of saving 1 life

- 33% of saving 100 lives

- 33% of saving 199 lives

All for the known cost of $10,000.

It would be an amazing intervention! If you run hundreds of similar interventions, you can save lives with cost-effectiveness of $100/life: the expected value is 100 lives saved, and the cost is always $10,000.

But here is what happens if you model it in Guesstimate:

You get $3400 mean cost per life! Changing the useful value by a factor of 34![1]

This is obvious in hindsight: since Guesstimate shows the "mean" cost-effectiveness

instead of what we care about, which is:

.[2]

Looking at the 5th and 95th percentile helps in many cases, but not in scenarios where there is a very small probability of very high effects and a significant probability of small effects. Minimal Guesstimate example with 4.8% of saving 1000 lives and 95.2% of saving 1 life.

Some practical examples of very small chances of huge value might be deworming or policy interventions. For those, mean(cost/effect) and mean(cost)/mean(effect) might differ by orders of magnitude.

Three recent examples:

- https://forum.effectivealtruism.org/posts/h2N9qEbvQ6RHABcae/a-critical-review-of-open-philanthropy-s-bet-on-criminal (search for "EDIT 22/06/2022:" in this post, it changes a result by an order of magnitude)

- https://forum.effectivealtruism.org/posts/RXm2mxvq3ReXmsHm4/ (in this case the difference is smaller, 54 vs 31, see https://colab.research.google.com/drive/1lnwjw2_zJHL4rBepw9yzAHQE0zL2ClDb?usp=sharing )

- https://forum.effectivealtruism.org/posts/9iBpokRpoJ2xspfnb/estimating-the-cost-effectiveness-of-scientific-research (19 vs 12, see https://colab.research.google.com/drive/1B_jnFGeUB_2fV7XR942QKJ_xyGMzvGMz?usp=sharing )

If you want to check another Guesstimate model

For most models, you can just manually calculate , since the means are shown in the Guesstimate UI.

For more complex cases, if you are comfortable with python, you can port a guesstimate model to numpy using https://recursing.github.io/guesstimate_to_squiggle/ and add .mean() liberally (very MVP, let me know if it doesn't work with a model you want to try).

Possible solutions / mitigations:

- If costs are constant in your model, consider looking at the value per dollar (or per $1,000) instead of dollars per value, so the denominator is constant. The minimal example would become https://www.getguesstimate.com/models/20682

Edit: this is by far the most favored approach in comments, and should cover most cases.

My view is that this is useful in part because huge uncertainties in costs are rare. - If you're interested in a single number for some sense of "expected cost-effectiveness", get the expected value and the expected cost and divide those numbers instead of the distributions (if the distributions can be considered independent).

- Other ideas? I'm definitely not an expert in any of this and there's probably a nice mathematical/statistical solution that I can't think of! Please comment if you think of anything!

Some questions I still have:

- How can we express the uncertainty around cost/effectiveness if the ratio distribution is hard to reason about and has misleading moments?

- How could the UI in guesstimate or some potential alternative indicate to the user when to use and when to use for nonlinear functions, to prevent people from making this very common mistake?

We might want to use the former for e.g. the value of cash transfers

Really curious to know if anyone has ideas!

Huge thanks to Sam Nolan, Justis Mills, and many others for fleshing out the main idea, editing, and correcting mistakes.

This work is licensed under a Creative Commons Attribution 4.0 International License.

- ^

Edit: this used to say "Underestimating the actual effectiveness by a factor of 34". But I don't think that this value is more "actual" than the other, just much more useful.

- ^

Assuming independence between cost and effect

Edit: several commenters pointed out that I'm implicitly considering

over many interventions, and it's not obvious at all that that's what we want in most cases.

I still think that's what we want in almost every case, but there's some interesting discussion going on in comments

I could be missing something but this sounds wrong to me. I think the actual objective is

mean(effect / cost).effect / costis the thing you care about, and if you're uncertain, you should take the expectation over the thing you care about.mean(cost / effect)can give the wrong answer because it's the reciprocal of what you care about.mean(cost) / mean(effect)is also wrong unless you have a constant cost. Consider for simplicity a case of constant effect of 1 life saved, and where the cost could be $10, $1000, or $10,000.mean(cost) / mean(effect)= $3670 per life saved, but the correct answer is 0.0337 lives saved per dollar = $29.67 per life saved.Ok, so say you have a fixed budget. Then you want to maximise mean(total effect), which is equal to mean(budget/cost * unit effect)

... I agree.

Also, infinite expected values come from having some chance of doing the thing an infinite number of times, where the problem is clearly the assumption that the effect is equal to budget/cost * unit effect when this is actually true only in the limit of small numbers of additional interventions.

Also, Lorenzo's proposal is ok when cost and effect are independent, while the error he identifies is still an error in this case.

The below is a reply to a previous version of the above comment.

I do not think we want to maximise mean("effect" - "cost").

Note "effect" and "cost" have different units, so they cannot be combined in that way. "Effect" refers to the outcome, whereas "cost" corresponds to the amount of resources we have to spend.

One might want to include "-cost" due to the desire of accounting for the counterfactual, but this is supposed to be included in "effect" = "factual effect" - "counterfactual effect".

We want to maximise mean("effect") for "cost" <= "maximum cost" (see this comment).

Yeah, I was mentally substituting "effect" for "good" and "cost" for "bad"

This was very common feedback, I should have added a section on it!

I disagree though. I think your example is perfect, with a denominator that spans many orders of magnitude

I disagree, let's say you have N interventions with that distribution of costs and effects and you fund all of them.

The total cost/effect would be ∑costi∑effecti=N⋅mean(cost)N⋅1=mean(cost)≈$3670

As an example, let's say you have three interventions with that distribution, and they turn out to be perfectly distributed, you have

total cost=$11,010 and total effect=3 lives so, as a funder that cares about expected value, $3670 is the value you care about.

https://docs.google.com/spreadsheets/d/1yfK7J5V4rBUQ7-lWKrdXDNyI3NYjRouub4KwO2PVkuQ/edit?usp=sharing here is a spreadsheet with 100 cases.

Not sure how useful it is as an intuition pump, but here is an even more extreme/absurd example: if there is a 0.001% chance that the cost is 0 and a 99.999% chance that the cost is $1T, mean(effect/cost) would be ∞, even if the effect is super tiny, which is definitely not what we care about.

In general, as JoelMcGuire mentioned, it's "a general issue where your simulation involves ratios", taking the other ratio helps only insofar as it prevents the denominator from spanning as many orders of magnitude.

Does this make sense? Is there a better way to write it? Is it completely wrong?

In general, I think we don't care about the mean of X/Y, (that indeed can be dominated by cases where Y is really tiny), but about the expected total X / Y.

That's true if you spend money that way, but why would you spend money that way? Why would you spend less on the interventions that are more cost-effective? It makes more sense to spend a fixed budget. Given a 1/3 chance that the cost per life saved is $10, $1000, or $10,000, and you spend $29.67, then you save 1 life in expectation (= 1/3 * (29.67 / 10 + 29.67 / 1000 + 29.67 / 10,000)).

That's a feature, not a bug. If something has positive value and zero cost, then you should spend zero dollars/resources to invoke the effect infinitely many times and produce infinite value (with probability 0.00001).

I agree a non-null probability of null cost implies infinite mean cost-effectiveness (mean ratio between effect and cost). However:

I think one should refer to "effect"/"cost" as cost-effectiveness, since more cost-effective interventions have greater ratios between the effect and cost.

Yeah, it's a very theoretical example.

There are things that could be modeled as very very low cost, like choosing A instead of B where both A and B cost $10, but indeed let's focus on the other example.

Using "effect"/"cost" helps in many cases, but definitely not in all.

E.g. for policy intervention estimates of costs can vary by orders of magnitude: see https://forum.effectivealtruism.org/posts/h2N9qEbvQ6RHABcae/a-critical-review-of-open-philanthropy-s-bet-on-criminal?commentId=NajaYiQD7KhAJyBcp

I think we care about the expected marginal cost-effectiveness (i.e. mean("marginal effect"/"marginal cost")). Both mean("total effect")/mean("total cost") and mean("total effect"/"total cost") are good approximations if our budget is small, but they might not be if the budget has to be large for some reason.

Haha, I came up with that example as well. You're thinking about this in the same way I did!

I think to say that one is the "actual objective" is not very rigorous. Although I'm saying this from a place of making that same argument. It does answer a valid question of "how much money should one donate to get an expected 1 unit of good" (which is also really easy to communicate, dollars per life saved is much easier to talk about than lives saved per dollar). I've been thinking about it for a while and put a comment under Edo Arad's one.

As for the second point about simple going E(cost)E(effect). I agree that this is likely an error, and you have a good counterexample.

I still don't think it's an error, added a comment with my perspective, curious to hear your thoughts!

Indeed it was common feedback, but I don't understand it fully, maybe we add a section on it to the post if we reach an agreement.

This is a recognised issue in health technology assessment. The most common solution is to first plot the incremental costs and effects on a cost-effectiveness plane to get a sense of the distributions:

Then to represent uncertainty in terms of the probability that an intervention is cost-effective at different cost-effectiveness thresholds (e.g. 20k and 30k per QALY). On the CEP above this is the proportion of samples below the respective lines, but it's generally better represented by cost-effectiveness acceptability curves (CEACs), as below:

Often, especially with multiple interventions, a cost-effectiveness acceptability frontier (CEAF) is added, representing the probability that the optimal decision (i.e. the one with highest expected net benefit) is the most cost-effective.

I can dig out proper references and examples if it would be useful, including Excel spreadsheets with macros you can adapt to generate them from your own data (such as samples exported from Guesstimate). There are also R packages that can do this, e.g. hesim and bcea.

This is super interesting, thanks! Exactly the kind of thing I was hoping for when posting this!

I hope it's well known inside EA as it's the first time I've seen it!

I think it might have some downsides though, or at the very least need some small modifications. If there is a policy intervention that has a fixed cost and a 5% chance of having a huge value, how would the curve look?

Also, what is "MAICER" in that plot?

After looking at this post score, the comments, and some discussions I'm having, I think I'm not the only person a bit confused about these things.

So I think any overview of these topics would definitely be useful, especially if it presents well-thought-out industry standards!

I would especially be interested in examples of how to use these tools in an EA context (even if very simplified and theoretical). But in general, having examples of different ways to look at these things I think can be very valuable!

MAICER = maximum acceptable incremental cost-effectiveness ratio. This is often called the willingness to pay for a unit of outcome, though the concepts are a little different. It is typically represented by lambda.

The CE plane is also useful as it indicates which quadrant the samples are in, i.e. NE = more effective but more costly (the most common), SE = more effective and cheaper (dominant), NW = less effective and more costly (dominated), and SW = less effective and cheaper. When there are samples in more than one quadrant, which is very common, confidence/credible intervals around the ICER are basically meaningless, as are negative ICERs more broadly. Distributions in Guesstimate, Causal, etc can therefore be misleading.

The standard textbook for heath economic evaluation is Drummond et al, 2015, and it's probably the best introduction to these methods.

For more details on the practicalities of modelling, especially in Excel, see Briggs, Claxton, & Sculpher, 2006.

For Bayesian (and grudgingly frequentist) approaches in R, see stuff by Gianluca Baio at UCL, e.g. this book, and his R package BCEA.

Cost-effectiveness planes are introduced in Black (1990). CEACs, CEAFs, and value of information are explained in more detail in Barton, Briggs, & Fenwick (2008); the latter is a very useful paper.

For more on VOI, see Wilson et al., 2014 and Strong, Oakley, Brennan, & Breeze, 2015.

For a very clear step-by-step explanation of calculating and interpreting ICERs and net benefit, see Paulden 2020. In the same issue of PharmacoEconomics there was a nice debate between those who favour dropping ICERs entirely and those who think they should be presented alongside net benefit. (I think I'm in the latter camp, though if I had to pick one I'd go for NB as you can't really quantify uncertainty properly around ICERs.)

For an application of some of those methods in EA, you can look at the evaluation we did of Donational. I'm not sure it was the right tool for the job (a BOTEC + heuristics might have been as good or better, given how speculative much of it was), and I had to adapt the methods a fair bit (e.g. to "donation-cost ratio" rather than "cost-effectiveness ratio"), but you can get the general idea. The images aren't showing for me, though; not sure if it's an issue on my end or the links are broken.

Here is a more standard model in Excel I did for an assignment.

Hope that helps. LMK if you want more.

Note that there are also methods for calculating confidence intervals around ICERs that avoid issues with ratios. The best I'm aware of is by Hatswell et al. I have an Excel sheet with all the macros etc set up if you want.

The derivation is wrong

First thing: unless I'm making a terrible mistake, your derivation for focusing on mean(cost)/mean(effect) is just mathematically wrong. It treats cost and effect as fixed numbers - you cannot divide a random variable by N because N isn't meaningful when talking about distributions. In the footnote you mention treating cost and effect as independent, which acknowledges that they are random variables, but then that invalidates the derivation.

Am I completely wrong? I can't see how this works.

This is not expected value - that could be bad

Second thing: do we actually care about mean(cost)/mean(effect)? In another comment you justify it because it's ∑cost/∑effect if we sum over different interventions. That does not mean it's the expected value of each intervention! It's just the total cost over the total effect. This does not have any direct link to expected value.

In fact, expected value is exactly why we don't want to squash variability in the variables. Let's say that cost is $1 or $1000 with 50% probability, and effect is 1 life or 1000 lives with 50% probability. Then mean(cost/effect) is 2 * 0.25 + 1000 * 0.25 + 0.001 * 0.25 ~250 $/life. Whereas mean(cost)/mean(effect) = $1/life.

Why are these so different? Because mean(cost)/mean(effect) neglects the "tail risk", the 25% chance that we spend $1000 and only save 1 life. This terrible situation is exactly why we do expected value calculations, because it matters and should be factored into our cost-effectiveness calculations.

That said, ∑cost/∑effect could have some philosophical grounding as a quantity we care about. I would love to see more elaboration on that in the post and a full defense of it. That would be really interesting and definitely worth a post to itself!

There are better solutions to unstable estimates

The best fix is: compute mean(effect/cost), not mean(cost/effect). This is because the denominator will never become zero. I have never seen a cost distribution that includes zero. It doesn't make sense for philanthropic applications. In fact if there was an intervention that had zero cost and improved lives we could all retire.

Yes, costs can still be low and this can make effect/cost very high. This is not a bug, it's a feature. This is what generates fat-tailed distributions of cost-effectiveness. The most cost-effective interventions have modest effects and very low costs.

I agree it's the main point of the post (we want to choose interventions in a way that maximizes the total effect). I thought it was a unanimous opinion but apparently, it's not?

I agree it helps in many cases, where the cost distribution spans fewer orders of magnitude than the effect distribution.

Sadly it doesn't solve all cases, E.g. for policy intervention estimates of costs can have uncertainty across orders of magnitude: see https://forum.effectivealtruism.org/posts/h2N9qEbvQ6RHABcae/a-critical-review-of-open-philanthropy-s-bet-on-criminal?commentId=NajaYiQD7KhAJyBcp

In the model in the post, both numerator and denominator have very high uncertainties

It's definitely not rigorous or formal.

I thought anyone with a math background would find the topic obvious, and most of the value would be in making the post accessible to casual estimators with many simple and informal examples.

My main argument for focusing on mean(cost)/mean(effect) is that I want to get the most value with a finite amount of resources, I don't really care about the EV of cost/effect since that's not valuable in itself. Maybe I could write total cost / total effect in that line, to keep it simple while making it less mathematically malformed?

I do not think anyone with a math background would find this obvious. Judging by the comments on this post and the feedback you said you received, I think you should update your beliefs on whether this claim is obvious at all.

In fact, I think the focus on examples detracts from the post. Examples can be misleading. Picking an example with a fixed numerator or a fixed denominator ignores the tail risk that I described in my comment, so the example serves to obscure and not explain.

I don't really understand why you think it's so common sense to focus on this quantity? Maybe given that you're proposing an alternative to expected value calculations it seems reasonable that you have the burden of explaining why it's a good alternative. I highly encourage you to make that as a separate post - I believe the title and content of this post are misleading given that you are proposing a new concept but rhetorically treating it like the one most EAs are used to.

Substantively speaking, one issue with total cost over total effect is that it is strictly a sampling quantity. For small N, we are never guaranteed that total cost = N * mean(cost). This is a consequence of the law of large numbers, not something you can take for granted. Unless we run hundreds of interventions there is a strong chance that total cost over total effect is not actually the same as mean(cost)/mean(effect), where mean() is taken as the true mean of the distribution.

It's okay for cost estimates to span many orders of magnitude. As long as they are not zero, mean(effect/cost) will be well defined.

I was completely wrong, indeed!

Will think about the comments for a few hours and write an appendix tonight.

Do you agree that the main practical takeaway for non-experts reading this post should be "Be very careful using mean(cost/effect), especially if the effect can be small"?

I disagree, the first example is exaggerated, but it's a very common issue, I think like a third of guesstimate models have some version of it. (see the three recent examples in the post)

Will respond to the other parts of the comments in the appendix, since many other commenters raised similar points.

I found this comment https://forum.effectivealtruism.org/posts/SesLZfeYsqjRxM6gq/probability-distributions-of-cost-effectiveness-can-be?commentId=nA3mJoj2fToXtX7pY from Jérémy particularly clear

I think the main practical takeaway should be to use mean(effect/cost) unless you have a really good reason not to. I agree mean(cost/effect) is a bad metric because it would be unreasonable for our effect distribution to not include zero or negative values - which is the only way mean(cost/effect) is even defined.

I think most people would agree that we want to maximise mean("effect") for "cost" <= "maximum cost". The crucial question is how to handle this optimisation problem when "effect", "cost" and "maximum cost" are distributions. The alternatives seem to be:

Thinking at the margin, these approaches seem equivalent.

Nice find, but I think there might be a subtle mistake there in the interpretation.

I think that the problem is with taking the expectation over 1effect, instead of multiplying the expected values mean(1effect)⋅mean(cost). It's reasonable to expect that the cost and the effect (of some specifically defined intervention) are uncorrelated, so the latter is actually the same as mean(costeffect).

However, taking the mean value of 1effect is definitely not the same as the reciprocal of the expected effect. In fact, at the start of the post you have computed a cost effectiveness of 100$ per life, but the way you have done it is by looking at the expected utility for the intervention (which is mean(effect)=100 lives ) and dividing the cost by this amount.

In GiveWell's CEAs (at least, I've verified for Deworm The World), they calculate the average value per constant constant cost. So this shouldn't affect their analysis.

I agree! It's the division that's not linear, not the multiplication.How do you think we could make it clearer in the post?

Edit: on more thought, I'm not sure I understand your point. mean(1/effect)⋅mean(cost) gives the "wrong" result (e.g. if effect can be 0 with non 0 probability, mean(1/effect) will be +∞)

Thank you so much for the post! I might communicate it as:

People are asking the question "How much money do you have to donate to get an expected value of 1 unit of good" Which could be formulated as:

E(good(x))=1

where x is the amount you donate and good(x) is the amount of utility you get out of it.

In most cases, this is linear, so: good(x)=goodcost∗x. And E(goodcostx)=1.

Solving for x in this case gets x=E(goodcost)−1, but the mistake is to solve it and get x=E(costgood).

Please correct me if this is a bad way to formulate the problem! Can't wait to see your future work as well

nice explanation :)

I think the question is:

This corresponds to the problem of maximising E(U(C)), where U(c) is the utility achieved (via a certain intervention) for the cost c (which must not exceed C). If the budget C is small enough (thinking at the margin):

Assuming U'(0) and C are independent, mean("effect"/"cost") equals mean("effect")/mean("cost"):

So, it seems that, regardless of the metric we choose, we should maximise E(U'(0)), i.e. the expected marginal cost-effectiveness.

Thanks for commenting here, and thanks again for your initial feedback!

I don't really have anything planned in this area, what would you be excited to see?

I think Michael Dickens explains this better than me in a more recent comment. The point is that we usually care about effect/cost rather than the other way around (although I'd love to understand more clearly why and when exactly that's true). In your example, you have implicitly computed this and then compare it to Guesstimate's model computing cost/effect.

Replied to Michael Dickens, curious about your thoughts! We should definitely add a section on this

I think your example should focus on the mean of the ratio between the effect and cost, not on the mean of the ratio between the cost and effect. The latter is a bad metric because:

The metric "effect"/"cost" has good properties:

Thanks for raising this question! Following other comment, I find the use of mean(cost)mean(effect) somewhat unsatisfactory.

Perhaps some of the confusion could be reduced by i) taking into account the number of interventions and ii) distinguishing the following two situations:

1. Epistemic uncertainty: the magic intervention will always save 1 life, or always save 100 lives, or always save 199 lives, we just don't know. In this case, one can repeat the intervention as many times as one wants, the expected cost-effectiveness will remain ~$3,400/life.

2. True randomness: sometimes the magic intervention will save 1 life, sometimes 100 lives, sometimes 199 lives. What happens then if you repeat it n times? If n=1, your expectation is still ~$3400/life (tail risk of a single life saved). But the more interventions you do, the more you converge to a combined cost-effectiveness $100/life (see figure below), because failed interventions will probably be compensated by very successful ones.

(R code to reproduce the plot :

X <- sample(1:20,1000000, replace=T) ; Y <- sapply(X,function(n)mean(10000*n/sum(sample(c(1,100,199), n, replace = T)))) ; plot(X, Y, log="y", pch=19, col=alpha("forestgreen", 0.3), xlab="Number of interventions", ylab="Cost-effectiveness ($/life, log scale)", main="Expected cost to save a live decreases with more interventions") ; lines(sort(unique(X)), sapply(sort(unique(X)), function(x)mean(Y[X==x])), lwd=3, col=alpha("darkgreen",0.5)))I'm not sure how to translate this into practice, especially since you can consider EA interventions as a portfolio even if you don't repeat the intervention 10 times yourself. But do you find this framing useful?

Thanks so much for writing this! I understood it much better than other comments.

I do! Especially the "epistemic uncertainty" vs "true randomness" framing I think is the core of the misunderstanding, I think we're usually in the second scenario (and funding lots of different interventions), but indeed it was a very implicit assumption!

Edit: you might be interested in this https://en.wikipedia.org/wiki/Ratio_estimator#Statistical_properties linked in another comment, for a formalization of the sample bias shown in the plot

This is a subtle point that people often miss (and I regularly forget!).

Also is a general issue where your simulation involves ratios. A positive denominator whose lower bound is close to zero will introduce huge and often implausible numbers. These are situations where the divergence between E(x) / E(y) and E(x/y) will be the largest.

This is my question too, mean(x) / mean(y) has no variance! The point of doing simulations was to quantify the uncertainty around our cost-effectiveness calculations!

The approach Sam (colleague at HLI) and I have taken is:

Edit: mean(x)/mean(y) has some variance, but it's not quite what we're after. Thank you Caspar Kaiser for pointing this out.

One possibility for quantifying the uncertainty of the cost-effectiveness is focussing on the metric "effect"/mean("cost"). It ignores the variance of "cost", but maybe this is not problematic given we want to maxime mean("effect") for a fixed (constant) "cost" we are willing to spend?

mean(x)/mean(y) is a contant, and therefore has null variance.

See this interesting comment from CasparKaiser (and my reply to it) for what he means by it.

Thanks so much for commenting! Huge fan of your work!

Yes, I think in general cases where the denominator spans multiple orders of magnitude (which is usually because it can be close to 0). In some models I saw it could even be negative (e.g. normal distribution with 90% between 1 and 10), which lead to even more confusing results.

Isn't that also misleading in many cases? e.g. mean(log(cash)) ≠ log(mean(cash)), and I think we care about the former.

I think if y does not vary too much on a log scale this is good enough, and that is true in most cases (not sure how to express this, has low relative variance?).

Otherwise, I guess you can try to consider y/x and still be informative (e.g. lives per $1,000 instead of dollars per lives).

Sad to hear you don't know of a good general solution :(

Do you think showing point clouds, like you do in the HLI reports, helps with this?

Isn't the variance 0? Since mean(x)/mean(y) is a number and not a distribution?

x/y does have some variance sometimes (e.g. a Cauchy distribution apparently has no variance, but the math seems harder than what we need).

Thanks again for your comment!

Hey!

No, I don't think that's correct. I take it that with "mean(x)" and "mean(y)" you mean the sample averages of x and y. In this case, these means will have variances equal to Var(x)/N and Var(y)/N. Consequently, the ratio of mean(x) and mean(y) will also have a variance. See here and here.

Thanks for commenting, this is interesting!

(For other people that had never heard of this and are curious about the derivation)

So the variance would be Var(¯X¯Y)=Var(∑X∑Y) which can be estimated running a simulation or with these fancy forumulas https://en.wikipedia.org/wiki/Ratio_estimator#Variance_estimates

But now I'm still confused: why is this "not quite what we're after" and why can't we use it to express the uncertainty around the cost/effectiveness ratio?But doesn't this tend to 0 if we consider enough samples? (N very large)

Cheers on getting around to writing this up!

Thanks so much for your feedback and help!

Just curious: Has anyone framed EA giving as a convex optimisation problem yet*?

Theres a number of posts like this on what feel like fairly obvious thing to me, so I wonder if there should be an educational series around it.

*(atleast ignoring knightian uncertainty)

The main reason why convex optimization isn't a commonly used model in this setting is because interventions are discrete objects. You can't run 1/4 of a malaria bednet project and 2/3 of a deworming project since there are scale effects.

When you treat projects as discrete and apply a budget constraint, the knapsack problem becomes a more natural model.

I might be misunderstanding what you mean by applying convex optimization. Say more?

Yup this is fair! I just realised this once I tried formalising.

Why would it be convex? Many opportunities have diminishing returns, which if I understand correctly would make the problem non-convex? E.g. the log(cash) example in the post

It is an optimisation problem, that's for sure 😅

I heard people model giving as a knapsack problem, considering choosing yes/no for fixed sized grant applications, but can't find anything about it on the forum and I don't know if it's particularly useful.

I agree that the idea in this post is fairly obvious to people that have some knowledge of statistics (but not to people like me that last thought about stats many years ago). I'm a bit annoyed that I can't answer the final two questions myself :/ Do you have any ideas?

If opportunities have consistently diminishing returns (i.e. the second derivative is negative), then it's convex. Giving opportunities may or may not actually be convex.

re: last 2 questions, I'm not immediately sure, sorry!

Having better educational content on the nature of the problem we're optimising would be useful.

Thanks for thinking about this

re: the topic being fairly obvious, apparently other comments think it's not obvious or even completely wrong, you might want to have a look at the discussion

I'll add a math formalisation if it helps!

I've made a major assumption in between though, about cost-effectiveness being strictly decreasing.

Assume you need to donate amount C across i opportunities, x_i is amount for i-th opportunity. Assume you need to donate now, and aren't considering saving for investment purposes or saving for future opportunities..

sum x_i = C

For i-th opportunity, let ΔU_i(x) map amount donated to utility gained. U_i could map scalar to scalar or scalar to a probability distribution over scalars. The delta sign indicates utility of the world after donation minus utility of the world if you burned the money instead. If you assume the second term is zero in your reference frame, then you can omit Δ sign for neatness.

We wish to maximise:

ΔU = sum ΔU_i(x_i)

U = sum U_i(x_i)

Assume there are no gained resources (monetary or otherwise) or information in each grant, besides the immediately obvious 1st order effect of the donation captured by the term U_i(x_i).

Assume U_i(x) is strictly increasing but with strictly decreasing slope.

U_i ' (x) > 0 for all positive x (more money donated is always good)

U_i '' (x) < 0 for all positive x (more money donated reduces cost-effectiveness)

Note this is a major assumption that does not always apply.

For instance, say malaria nets cost $2 each and some constant number saves a life. Then U_i(x) appears to be a linear function, which satisfies this. But in practice, donating 2 cents more does not lead to 1/100th of a malaria net. So U_i(x) is actually a function that looks like a staircase making a tiny step every $2. This does not satisfy above conditions. So that condition does not apply. However, we can approximate it as linear as $2 is very small.

We cannot approximate a step function or staircase as linear if it only generates utility in response to very large costs.

Now we can approximate U_i(x) as linear in a small region around x=x_i

U_i(x) = y_i * x_i

for some constant y_i

y_i is the cost-effectiveness, it is also the slope of the function U_i(x)

We may have a probability distribution over y_i, instead of a known constant y_i.

We can now use a greedy algo (*) to take decisions. Assume we split our large amount C, into tiny amounts c to donate one at a time.

For each c, we have:

Maximise sum y_i * x_i subject to sum x_i = c

The solution is to just allocate x_i = c for whichever y_i is largest, and all other x_i = 0

Once you've done this you can calculate the new cost-effectiveness values and then repeat the process. You'll have to run many iterations of the algo until you donate the whole amount C.

If y_i is indeed a probability distribution, then we have

Maximise E(sum y_i * x_i) = sum x_i * E(y_i) subject to sum x_i = c

Here we can indeed take the expected cost-effectiveness of each opportunity.

(*) We can do this only if all U_i are strictly increasing with strictly decreasing slope I think.

A simplified (oversimplified?) version of this is here.

Will check!

Just checked knapsack problem and yup this seems super useful.

re: convexity, maybe I am making the wrong assumption that all opportunities will have diminishing cost-effectiveness as more money pours into them. It is possible there are some opportunities that become more cost-effective* once some initial money has been poured in and groundwork has been done.

*Ideally you can factor in all those new opportunities opening up into the "effect" term of the original grant, then you again get diminishing cost-effectiveness I think. But I don't know if that can always be done in practice due to uncertainty.

I think most people make this assumption. If that's all you mean by convex optimization then I think current heuristics are optimizing. In particular, "donate to givewell top charities until something is more cost effective than them" is basically using concavity of the cost effectiveness function.