Last updated 2023-01-06 to update fee minimums.

A donor-advised fund (DAF) is an investment account that lets you take a tax deduction now and give the money to charity later. When you give money to a DAF, you can deduct that money just as you would deduct a charitable contribution. The DAF invests the money tax-free. At any time, you can direct the DAF to donate some or all of its holdings to the charity of your choice.

You can open a DAF through a donor-advised fund provider. A provider charges an administrative fee to invest your DAF and make donations in accordance with your recommendations.

For donors in the United States, which DAF provider is the best?

The short answer:

All of the big DAF providers offer similar features. For most people, it doesn't really matter which one you choose.

- If you already have a DAF, you might as well keep using it.

- If you have a brokerage account at Fidelity, Schwab, or Vanguard, then the easiest thing to do is to open a DAF with your brokerage account. That way, you can manage all your investments in one place.

Otherwise, I believe Schwab Charitable is the best DAF provider for most people.

The long answer:

Even if all the major DAF providers are reasonably good, they do have their own strengths and weaknesses. In the rest of this post, let's look at how they compare.

Cross-posted to my website.

My process

I made a list of every United States nationwide DAF provider I could find. I excluded regional DAF providers (example: Silicon Valley Community Foundation), providers that weren't cause-agnostic (example: National Christian Foundation), and providers that don't work with individual donors (example: American Online Giving Foundation). Your local community foundation might offer a better DAF than any of the national providers of my list, but there are too many community foundations for me to look at them all.

I ended up with eight DAF providers (in alphabetical order):

- American Endowment Foundation (AEF)

- Charityvest (see disclaimer)

- Fidelity Charitable

- Greater Horizons

- National Philanthropic Trust (NPTrust)

- Schwab Charitable

- T. Rowe Price Charitable

- Vanguard Charitable

This list is probably not comprehensive, but it's all the DAF providers I could find that meet my criteria.

I spoke to representatives at these providers to get more information about their offerings. I also spoke to a few financial advisors who manage DAFs at different providers.

I then eliminated four DAF providers:

- T. Rowe Price Charitable has the most investment options, but most of the funds have expense ratios of 0.6% or higher. Not worth it unless you really want those extra investment selections.

- AEF and NPTrust both look like decent options, but they charge higher administrative fees than Vanguard/Schwab, offer a worse user experience, and don't have any special features to compensate. So we might as well exclude them.

- Fidelity is nearly identical to Schwab, but it offers fewer investment options, so let's exclude it.

Four DAF providers remain: Charityvest, Greater Horizons, Schwab, and Vanguard.

Caveat 1: I don't have good firsthand knowledge of any of these eight DAF providers except for Fidelity Charitable, which I used to use, and Greater Horizons, which I currently use. I created accounts at Charityvest, Schwab, and Vanguard to get a sense of how they work, but I haven't tried to do anything fancy like set up an advisor-managed account. I had to make subjective judgments on things like UI, so don't take my claims as definitive.

Caveat 2: This article is not about whether you should open a DAF in the first place. For some people, a foundation would better serve their needs; other people should simply keep their money in a taxable account. But if you've already decided you want a DAF, I hope this article will help you choose a provider.

Comparison

Let's compare Vanguard, Schwab, Greater Horizons, and Charityvest on six questions:

- What fees do they charge?

- Do they have contribution/grant minimums?

- What pre-selected investment options do they provide?

- How flexible are their advisor-managed accounts?

- Can you contribute complex assets such as cryptocurrency or real estate?

- How good is the user experience?

Fees

- Vanguard has a minimum annual fee of $250.

- Schwab has no minimum annual fee.

- Greater Horizons has a minimum annual fee of $500

- Charityvest has a minimum annual fee of $48 ($4 per month).

Vanguard, Schwab, and Charityvest offer tiered fee structures based on the value of the account. Greater Horizons has a similar fee structure, but I cannot provide a link because the fees are not publicly available. See Appendix for full details on the administrative fees for each provider.

In brief:

- Charityvest charges the lowest (or tied-for-lowest) fees at every account size.

- For account sizes under $25,000, Schwab is the second cheapest.

- For account sizes between $25,000 and $1 million, the other three providers (Greater Horizons, Schwab, Vanguard) charge the same fees.

- For larger accounts, Vanguard is the cheapest after Charityvest; Schwab and Greater Horizons cost about the same. But the differences are fairly small, and they all charge much lower fees on large accounts than on small accounts.

These four providers' fees do not differ greatly, although Charityvest is notably cheaper than the other three.[1]

Minimums

Donor-advised funds have three types of minimums:

- Minimum account size / initial contribution

- Minimum additional contribution

- Minimum grant size

| Charityvest | Greater Horizons | Schwab | Vanguard | |

|---|---|---|---|---|

| Account Min | $0 | $0 | $0 | $0 |

| Contribution Min | $20 | $0 | $0 | $5,000 |

| Grant Min | $20 | $0 | $50 | $500 |

Investment options

Let's compare the investment options for Charityvest, Greater Horizons, Schwab, and Vanguard.

They offer index funds covering the following markets:

| Charityvest | Greater Horizons | Schwab | Vanguard | |

|---|---|---|---|---|

| US stocks | Y | Y | Y | Y |

| US small-cap | Y | |||

| international stocks | Y | Y | Y | Y |

| Europe stocks | Y | |||

| Pacific stocks | Y | |||

| emerging market stocks | Y | Y | ||

| US bonds | Y | Y | Y | Y |

| international bonds | Y | Y | ||

| TIPS | Y | |||

| money market | Y | Y | Y | Y |

The expense ratios on the funds themselves are low enough not to matter as long as you stick with the passively-managed funds. (Vanguard and Schwab both offer a few actively-managed funds with higher fees.) You can use any of the three providers to construct a globally diversified portfolio for an average expense ratio of about 0.05%.

Vanguard and Charityvest investors can approximately replicate the global market portfolio with 30% US stocks, 30% international stocks, 20% US bonds, and 20% international bonds. Investors with Schwab or Greater Horizons don't have access to international bonds, so the closest they can get is something like 30% US stocks, 30% international stocks, 40% US bonds.

Vanguard and Charityvest offer a few ESG funds with low expense ratios. Schwab also has ESG funds, but they're unreasonably expensive.

- If you want the global market portfolio, use Vanguard or Charityvest because they offer an international bond index.

- If you want ESG funds, use Vanguard or Charityvest.

- If you want to invest in a specific market that only one provider offers, use that provider.

- Otherwise, any provider is a good choice.

Advisor-managed accounts

Schwab and Greater Horizons allow donors to appoint an investment advisor who can invest in things other than the pre-selected funds. Their program guidelines (links: Greater Horizons, Schwab (p. 11–14)) dictate what investments are allowed.

Vanguard does not allow advisor-managed accounts. Charityvest allows them, but only for accounts with at least $1 million.

Some examples of restrictions that apply to these accounts:

- "Risky" investments are not allowed, including margin, short sales, options (except covered calls/puts), futures, and swaps, unless held within a mutual fund or ETF structure.

- The advisor must not charge higher fees to the DAF than to the donor's personal accounts.

- The donor's family members may not serve as investment advisors.

Schwab has some additional restrictions that the others do not share:

- The account must trade using a Schwab brokerage account.

- The advisor must establish a benchmark and then track that benchmark reasonably closely. If the account deviates substantially from the benchmark, the advisor is accountable to Schwab's investment committee.

- The account must meet certain asset allocation requirements. For example, it cannot allocate more than 25% to any one security, more than 25% to emerging market equities, or more than 50% "to publicly traded funds that pursue alternative or non-diversified investment strategies, e.g., commodities or cryptocurrencies".

- Advisors may not invest in funds that they own or manage.

Greater Horizons provides the most flexibility to investment advisors. If I wanted to do anything unconventional, I would use Greater Horizons. (Actually, I do use Greater Horizons for exactly this reason.)

Contributing complex assets

Greater Horizons, Schwab, Charityvest, and Vanguard can all accept various types of complex assets, including cryptocurrency, private equity, real estate, and more.[2]

These providers claim to accept pretty much any type of asset that can legally be donated. But if you want to donate a large position in a complex asset, you should contact a DAF provider before opening an account to confirm that they can receive it.

These providers all manage donations of complex assets through the same third party[3] (Charitable Solutions LLC).

(Amusingly, AEF, NPTrust, and Schwab all say they're "uniquely flexible" when handling complex assets. If they're all uniquely flexible, I guess that means none of them is?)

User experience

Most donors probably only care about the basic features of a DAF—they don't need fancy investment options or the ability to contribute complex assets. And the good DAF providers all charge similar fees. So most people should go with whichever DAF provider offers the best user experience.

Of the four providers I'm focusing on, Greater Horizons easily has the worst sign-up process. You have to request that a customer service representative reach out to you. Then they send you a PDF form to fill out, and create the account manually after you fill out the form. In contrast, Charityvest, Schwab and Vanguard all let you sign up online and you can fill out your personal information on the website.

In the process of writing this article, I created accounts at Schwab, Vanguard, and Charityvest and went through a few common use cases. I found them all easy to use. Charityvest and Schwab were slightly simpler than Vanguard.

Another important aspect of user experience is the quality of customer service. Good customer service matters, but it's also difficult to assess—if you have a good/bad customer service experience, that might have more to do with the specific person you talked to than the quality of service in general. That said, I spoke over email and over the phone with all four providers to get my questions answered, and I had good experiences with all four. I don't know if my experience with Charityvest would generalize because the CEO specifically reached out to me to ask me to review it (see disclaimer).

I've heard that Schwab (the investment broker, not the DAF provider) has particularly good customer service, and the service of Vanguard (the investment broker) isn't as good. But Schwab Charitable/Vanguard Charitable operate largely independently from Schwab/Vanguard, so that might not apply. For example, Schwab provides a 24/7 phone number and a 24/7 live chat, but Schwab Charitable's customer service is only available during business hours, and it only has phone and email, no live chat.

If you already have a brokerage account at Vanguard/Schwab, then it makes sense to open a DAF with Vanguard Charitable/Schwab Charitable (respectively) to keep all your accounts in one place. Otherwise, both provide good user experiences, with a slight edge for Schwab.

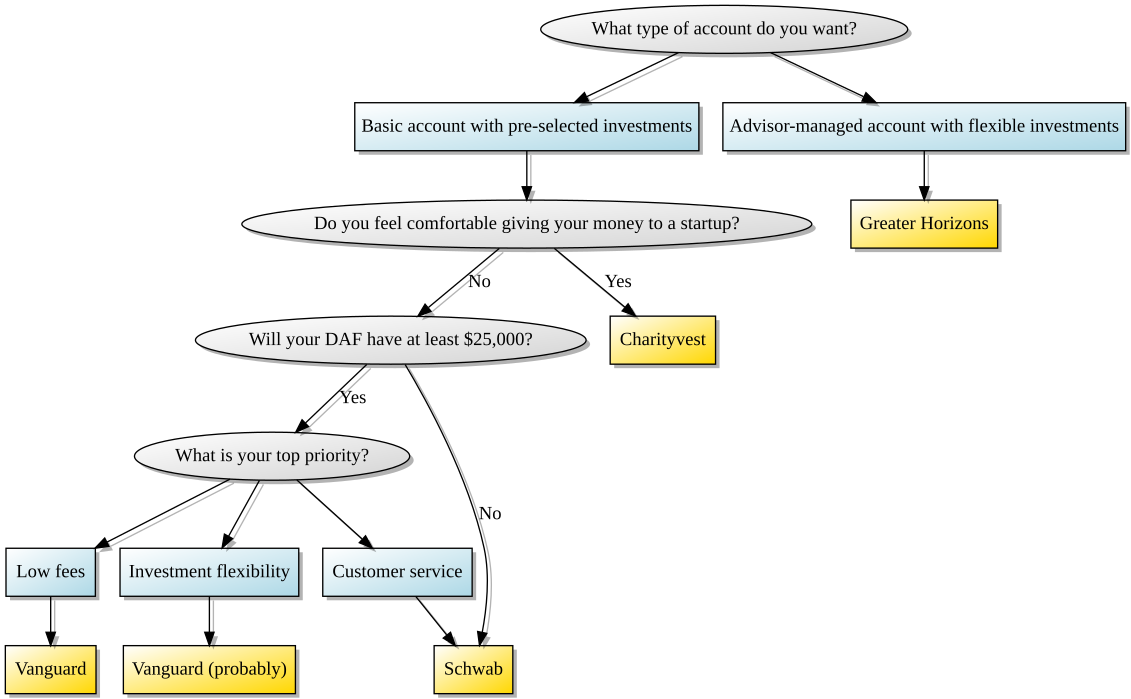

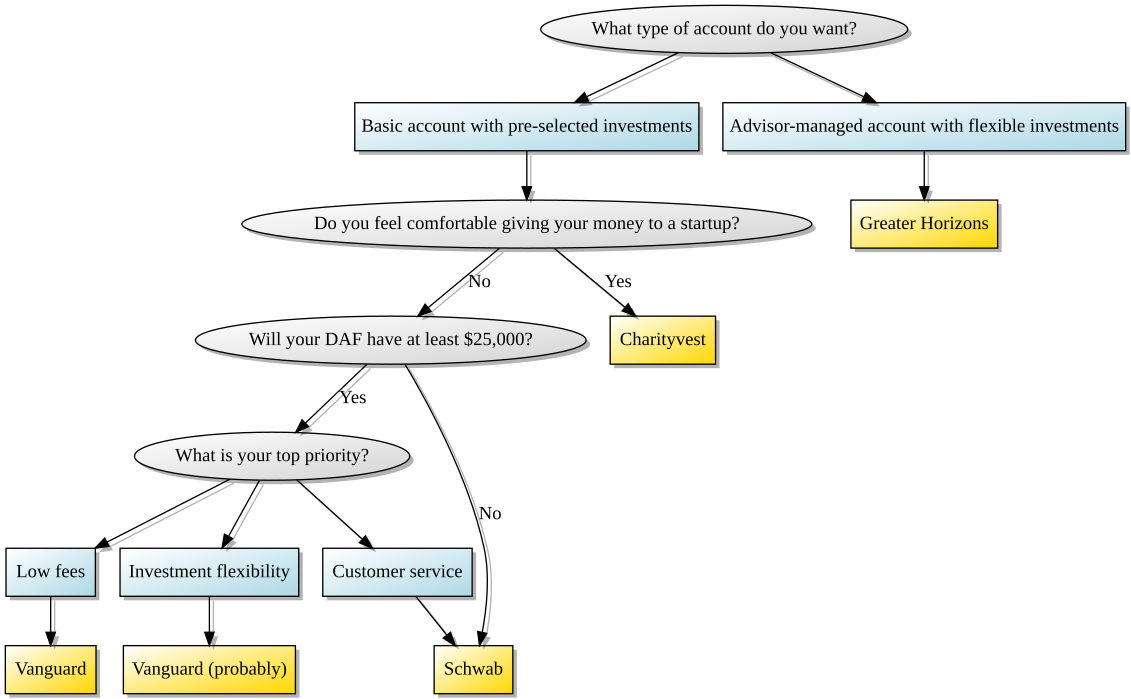

The best DAF provider(s)

This flow chart shows the best DAF provider depending on your circumstances:

(Click here for the full-size image.)

{kind=link}

A text summary of this flow chart:

- If you want an advisor-managed account, use Greater Horizons.

- If you feel comfortable giving your money to a startup with an unproven track record, use Charityvest.

- If your DAF will have less than $25,000, use Schwab.

- Otherwise, choose a DAF provider based on your top priority:

- Low fees = Vanguard

- Investment flexibility = probably Vanguard (depending on what investments you want, see Investment options for details)

- Customer service = Schwab

Vanguard and Schwab have identical fees for accounts with up to $1 million, so low fees should only be your top priority if your DAF will have more than that.

Purely in terms of features, Charityvest looks like the best provider—it has the lowest fees and offers a wide range of investment options. But I would hesitate to use it because it's new—it only launched in 2021, and didn't allow investments until 2022. This introduces significant risks. For instance, if Charityvest can't earn enough money to sustain itself, it might have to dissolve donors' accounts and use their money to pay its bills (which it has a legal right to do, and donors would have no recourse). So in spite of the upsides, I would not use Charityvest unless I became more confident in its financial stability.

This flow chart only includes Charityvest, Greater Horizons, Schwab, and Vanguard. That's not because I believe these four are better at everything than the other four providers I didn't discuss. For example, I think Fidelity has a better UI than Vanguard, and NPTrust offers more flexibility than Schwab for advisor-managed accounts. Rather, I chose these four because each one is the best at something, while the other four are not the best at anything (in my estimation).

More on Fidelity, AEF, NPTrust, and T. Rowe Price

Since I didn't compare them in detail, here are my impressions of the other four DAF providers, ranked from worst to best:

- T. Rowe Price Charitable is too expensive to be worth using. The other DAF providers on my list are all basically fine, but if you have an DAF at T. Rowe Price with a decent amount of money, you should consider switching to a new provider.

- AEF and NPTrust seem adequate, but they have a few issues:

- They're more opaque than the other DAF providers, and I had a harder time getting them to tell me what I wanted to know.[4]

- They make it more difficult to set up an account.

- For advisor-managed accounts, they impose more restrictions on the investment advisor than Greater Horizons does.

- They charge somewhat higher administrative fees than Fidelity/Schwab/Vanguard.

- NPTrust's pre-selected investment funds are too expensive. NPTrust should only be used with an advisor-managed account. AEF does not have pre-selected funds—you must appoint an investment advisor.

- AEF's website is so buggy that it's unusable on Firefox. Even ignoring the bugs, AEF's UI is much worse than Fidelity/Schwab/Vanguard.

- Fidelity Charitable is as good as Schwab/Vanguard for most purposes. I like it better than T. Rowe Price, AEF, or NPTrust. I like Fidelity a little bit less than Schwab because it provides fewer investment options and the UI is slightly harder to use[5], but Fidelity still seems like a fine choice.

Bonus fact: If you have at least $5 million, Fidelity Charitable lets you manage your own investments (without an advisor). I don't believe any of the other DAF providers let you do this.

Disclaimer on Charityvest

I learned about Charityvest when their CEO, Stephen Kump, emailed me to ask me to review it prior to its public launch. He gave me access to the beta (which I used to check out Charityvest and see how I liked it) and added $20 to my account (which I did not use, to avoid any conflict of interest). I did not receive any other compensation for writing about Charityvest. I edited this article to include Charityvest because I believed it had some advantages over other DAF providers. Everything I wrote about it is my own opinion.

Appendix: Table of administrative fees

Fees can be found at these links: AEF[6], Charityvest, Fidelity, NPTrust, Schwab, T. Rowe Price, Vanguard.

Greater Horizons does not publish its fees online. I learned what it charges by speaking to a representative. I don't like it when companies don't publish their fees, but I will respect Greater Horizons' preferences by not disclosing them. If you want to know the specifics, contact them directly.

Minimum fees:

| AEF | Charityvest | Fidelity | NPTrust | Schwab | T. Rowe Price | Vanguard | |

|---|---|---|---|---|---|---|---|

| Minimum Fee | $500 | $48 | $100 | None | None | None | None |

Tiered fees:

| Account Value | AEF | Charityvest | Fidelity | NPTrust | Schwab | T. Rowe Price | Vanguard |

|---|---|---|---|---|---|---|---|

| First $250K | 0.70% | 0.45% | 0.60% | 0.85% | 0.60% | 0.50% | 0.60% |

| Next $250K | 0.70% | 0.45% | 0.60% | 0.70% | 0.60% | 0.50% | 0.60% |

| Next $500K | 0.35% | 0.25% | 0.30% | 0.60% | 0.30% | 0.39% | 0.30% |

| Next $1.5M | 0.25% | 0.10% | 0.20% | 0.45% | 0.20% | 0.18% | 0.13% |

| Next $2.5M | 0.15% | 0.10% | 0.15% | 0.25% | 0.15% | 0.12% | 0.13% |

| Next $5M | 0.15% | 0.10% | 0.15% | 0.13% | 0.10% | 0.13% | |

| Next $5M | 0.15% | 0.05% | 0.10% | 0.12% | 0.10% | 0.13% | |

| Next $15M | 0.10% | 0.05% | 0.10% | 0.10% | 0.09% | 0.10% | |

| Over $30M | 0.10% | 0.05% | 0.10% | 0.10% | 0.09% | 0.05% |

Note: Fidelity uses a flat fee schedule on accounts with over $5 million, so its fees are not directly comparable to the others.

Some observations:

- Charityvest is cheapest or tied for cheapest at every level.

- T. Rowe Price has the 2nd lowest administrative fees, but its investment options charge high expense ratios. It only offers one reasonably-priced fund (an S&P 500 index fund). T. Rowe Price only has the 2nd lowest all-in fee if you invest in the S&P 500 and nothing else.

- Even though Schwab has lower fees than Vanguard at one tier, there is no account value at which Vanguard has a higher total fee.

- Even though NPTrust has lower fees than Schwab at one tier, there is no account value at which Schwab has a higher total fee.

- Fidelity's flat fee structure above $5 million means that near the bottom of a tier (e.g., $11 million), it's cheaper than Schwab or Vanguard, and near the top of a tier (e.g., $19 million), it's more expensive.[7]

Notes

According to the Cliff Asness fee classification, Charityvest's fee improvement is "ok but not huge". ↩︎

Vanguard's website does not state that they can accept cryptocurrency, but I confirmed with a representative that they take donations of cryptocurrency if the value of the contribution is at least $50,000. ↩︎

AEF, Fidelity, and NPTrust also use Charitable Solutions LLC. It seems that Charitable Solutions LLC has something of a monopoly on managing donations of complex assets. ↩︎

My incredible customer service experience with NPTrust:

- I send them an email to ask what types of investments they allow.

- A representative replies and says we need to set up a phone call.

- On the phone call, I repeat my question. They then email me a PDF that contains their investment requirements.

I'm tempted to send them one of those "this meeting could have been an email" coffee mugs. ↩︎

Fidelity's and Schwab's UIs are nearly identical. The only real difference I noticed is that Schwab does a better job of conglomerating your accounts. If you have both a brokerage account and a DAF at Schwab, you can easily switch between them from the landing page. If you have both types of accounts at Fidelity, you can navigate to your DAF from the landing page, but it sends you to a separate URL and sometimes requires you to log in again. ↩︎

AEF does not provide a fee schedule, only a fee calculator. I used the calculator to reverse-engineer the fee schedule. ↩︎

For the mathematically inclined, this function converts Fidelity's flat fee into an equivalent tiered fee on amounts over $5 million, given two variables

AUMandflat_fee:

↩︎tiered_fee = ((AUM * flat_fee) - $11,250) / (AUM - $5,000,000)

Does this apply to US only? If so, could be good to say at the very top.

(I haven't read the post, but I'm very excited that such a resource exists!)

Also, if anyone is up for it, I think a resource for DAF providers in other countries would seem useful as well

Yeah this is for US only. I actually thought I had said that in the post, but looks like I forgot to! I'll edit it.

You said it in the "My process" section, but not earlier.

Great post. One more resource that EAs should be aware of is Charitable Solutions LLC. They facilitate large (>$250k) DAF donations of exotic assets like restricted stock, LP interests, art, etc.

This looks really useful, many thanks for the writeup. I'd note that I've been using Vanguard for regular investments and found website annoying and the customer support quite bad; there would be long periods where they wouldn't offer any because things were "too crowded". I think most people underestimate the value of customer support, in part because it is most valuable in the tail end situations.

Some quick questions:

- Are there any simple ways of making investments in these accounts that offer 2x leverage or more? Are there things here that you'd recommend?

- Do you have an intuition around when one should make a Donor-Advised Fund? If there are no minimums, should you set one up once you hit, say, $5K in donations that won't be spent a given tax year?

- How easy is it for others to invest in one's Donor-Advised Fund? Like, would it be really easy to set up your own version of EA Funds?

"Do you have an intuition around when one should make a Donor-Advised Fund?"

The reason I, personally, opened a DAF was to make it dead simple to donate appreciated stock.

If you're not familiar: you can give a lot more to charity, at the same cost to you, if you gift stock that's gone up in price instead of cash. For example, say you bought stock for $1k and has appreciated to $10k. (Lucky you!) If you sold it to donate it to charity, you first have to pay capital gains tax on the $9k, which is 35% or about $3k. So the charity only gets $7k. If instead, you gift the stock directly: you don't pay taxes, and neither does the charity. Basically, the US Govt matches your donation. Great deal, right?

The catch is: actually gifting stock is really annoying! When I was donating TSLA shares to GiveWell I had to literally fax a piece of paper telling them which shares to take out of my account. A DAF is much simpler; I just click some buttons from my Schwab investment account and the stock lands and gets sold in my Schwab Charitable DAF. There are other great reasons to open a DAF too -- but making this tax optimization really easy is why I went for it.

DAFs do make it much easier to donate appreciated stock, and this is good advice. However, if you want to make a donation of appreciated assests and you aren't able to set up a DAF, EA Funds accepts donations of stock (in the US) and cryptocurrency (US, UK, and NL) for donations of more than $1000 (no promises that you won't have to send a fax to your broker if you want to donate stock, but in general that hasn't been the case for most of our donors who are donating from Vanguard etc).

Thanks for sharing your experience with Vanguard! That aligns with anecdotes I've heard about Vanguard's brokerage service.

I just published something about DAF investing strategies: https://mdickens.me/2021/04/06/investing_strategies_DAF/ In this section, I talk about leveraged ETFs. I believe the only way to invest with leverage in a DAF is through a leveraged ETF or mutual fund, although I've heard conflicting things about what the actual legal requirements are. In general, I don't think leveraged ETFs are good investments.

If you want to use leverage, probably never. (Or just use it to convert stock into cash for donations, as akrolsmir described.) Otherwise, you want to have at least $10,000 or so, otherwise the minimum fee will eat too large a % of your assets each year. (Schwab and Fidelity both have a $100 minimum fee.)

It's definitely possible. I personally don't have my own DAF, I use my parents' DAF. I'm a full authorized user on the account, which means I had to connect my Fidelity account to the DAF. If you don't care about managing anything and just want to donate to the DAF, I would think that should be pretty easy, but I haven't tried it. I think it should be as simple as writing a check to Fidelity Charitable with a note that the money is for that particular DAF.

One important factor when looking for a DAF is whether it restricts your donations to only public charities as defined by the IRS and will not let you direct donations to private foundations. Both of these can be approved as 501(c)3) non-profits. I believe the vast majority of non-profits are classified as private foundations. My son started a non-profit that was initially classified by the IRS as a private foundation. He can file in a future year after having actual experience and try to get classified as a public charity. In his initial fund raising several of our friends with DAF's could not use their funds to make donations while other friends using other providers were allowed to make donations to his private foundations. I have my own 501(c)(3) private foundation and I can donate to any approved non-profit, public or private. Investment options, fees and customer service are all important but the real value is in making donations to the charities you want to support.

Public charity status is the norm -- most charities should be able to achieve it fairly easily unless perhaps dependent on a very small number of donors for the bulk of funds.

Thanks so much for this great post! I've had Schwab Charitable for about a year now, and has been very smooth. Also potentially worth noting, one can transfer between DAFs across various providers, so if the size of a DAF were to change, I think it should be feasible to move to one with better options/fees as needed.

You may want to correct your Vanguard fee schedule; they charge a $250 “maintenance fee” on account balances under $25,000. This appears to be on top of the 0.60% fee, meaning that accounts that ultimately decline in value suffer total annual fees bordering on ~2% . This seems to make Schwab a much better option for accounts that may ultimately decline below $25k, right?

See “Maintenance Fee” at https://www.vanguardcharitable.org/company-policies/policies-and-guidelines

Thanks for pointing this out! I updated the post.

Schwab also told me (in Nov 2020) that they only accept cryptocurrency if the contribution is >$50,000, and their vendors charge a 1% fee on Bitcoin and a $3,500 flat fee for Ethereum. I spoke to Fidelity Charitable who told me they had no minimum contribution for cryptocurrency, but I didn't inquire about fees.

FYI @MichaelDickens I just heard from Vanguard Charitable:

> At this time, Vanguard Charitable only accepts contributions of Bitcoin and Bitcoin Cash that are valued over $100,000.00.

Might be worth mentioning in the post.

Just got off the phone with Fidelity Charitable, they accept ETH with no minimums. (Also the two agents I spoke to were smart and efficient, average wait time of 8 min)

another relevant minimum is minimum account activity—have you or others incorporated this into your comparisons? for example, it looks like fidelity requires disbursement of 5% of net assets per year (averaged over 5 year periods), whereas vanguard requires at least one $500 grant every 30 months.

Where are you getting that info? I thought Fidelity Charitable had no distribution requirement. Distribution requirement is definitely relevant if there is one.

fidelity: their "open an account" page (https://www.fidelitycharitable.org/open-account.html) directs to their program guidelines (https://www.fidelitycharitable.org/content/dam/fc-public/docs/programs/fidelity-charitable-program-guidelines.pdf), with the relevant info on page 17. on closer inspection, it looks like disbursement of 5% of net assets per year could be a policy for fidelity charitable as a whole, not necessarily for each individual account. even so, they claim to require active grantmaking and say they will start making grants from any account that hasn't disbursed anything for two years (top of page 18). i don't know if this policy is commonly applied, but at the very least it's a risk.

vanguard: their "open an account" page (https://www.vanguardcharitable.org/open-an-account/consent/) has a link to their policies and guidelines, with the relevant information under heading "minimums, timing, and amounts", subheading "minimum account activity".

i didn't see any minimum activity info on the schwab website and haven't had a chance to check others.

After a number of years Fidelity required me to make a $50 disbursement, so I think this requirement might be de minimis.

Can you clarify why you'd create a DAF instead of just donating directly to a high-impact charity? Using EA Funds as a baseline, I'd be interested in what value a DAF provides over just donating there.

That's a complicated question, but in short, if you believe that there will be better donation opportunities in the future, you might use a DAF.

Fantastic analysis, wish I had this prior to making my decision. Back in the day both Fidelity and Schwab had a $5K minimum and Fidelity had a $50 minimum contribution whereas Schwab had a $500 minimum, which is why I went with Fidelity. Glad to see they made these improvements.

Going off of Dan's comment, if a Fidelity (or Schwab) account is at $25K or more, would you recommend switching over to Vanguard given the better fees and investment options?

Unless you're putting a lot of work into optimizing your DAF investments (like I describe here), Fidelity is pretty much just as good as Vanguard.

Love that you’re writing a comprehensive write up about navigating DAFs, Michael.

Another one I’ll put on your radar is Groundswell (www.groundswell.io).

Full disclosure, I work for them and I would consider it comparable to Charityvest in regards to price and the ability to accept stock.

We are focused on offering DAFs as an employee benefit, although anyone can download and use Groundswell as they would with Charityvest.

Excellent, helpful and concise, thanks so much Michael! Perhaps include a minimum balance line to your Appendix just under "minimum fees" section. As you noted, Vanguard has a $25k minimum balance, effectively making their minimum annual fee $150. Fidelity has no initial minimum deposit and no minimum balance, which may be helpful when opening an account and managing large grants that bring the account balance below the minimum between contributions.

This was really helpful, thank you!