EXECUTIVE SUMMARY

Within animal advocacy, corporate campaigns have become an important and widely used tactic as evidence of their efficacy has accrued (Šimčikas 2019; Philanthropy 2016; Sarek 2019a, [b] 2019). These campaigns allow the movement to leverage a relatively small amount of funding to disrupt and apply large amounts of pressure onto corporations with the intention to achieve policy change. The asks for these anti-corporate campaigns can come in several forms; from more simplistic singular asks such as the cage-free campaigns, to more complicated composite asks which include several elements such as the Better Chicken Commitment (“The Better Chicken Commitment Policy” n.d.). From our previous research into the asks used in such corporate campaigns, we identified a foundational uncertainty in their construction. Namely, how much should we ask for? The more additional elements incorporated into the ask, the greater the potential benefits to the animal we are trying to provide improved protections. However, as more elements are added, the greater the investment required by the companies targeted, and the more difficult it becomes to communicate the ask to the public and the companies’ decision makers.

In this report, we examine the fundamental theories behind how these campaigns work and the factors determining their success. Ultimately we view corporate campaigns as a form of extortion, where interest groups threaten companies with either supply chain disruption, or more commonly, reputational damage if they do not comply with their demands. We find that if companies experience anti-corporate campaigns or suffer from other similar revelations of unethical business practices, this information can have significant lasting damage to their market capitalisation and financial performance. Thus, companies should be willing to invest significant resources to mitigate this risk. It is possible to model this decision from a rational economic point of view where corporations should be willing to pay up to the potential damage to avoid a campaign. However any attempts to do so should be understood within the specific context of that corporation's decision-making and in light of the large amount of uncertainty involved. As corporate campaigns are ultimately a social phenomena, precise quantitative estimates are not reliable, but various research methods can be used to make more informed decisions on the magnitude of the ask that can be made. To better inform future decision makers in ask formation, we should combine this sort of analysis with scoping the specific context of the campaign including the supply chain, key stakeholders and their motivations.

HOW DO CORPORATE CAMPAIGNS WORK?

Corporate campaigns are a strategic effort by an interest group to put pressure on or cooperate with a company to improve their organisation's policies. These interest groups can come from within the company, as is the case with labour unions, or external movements that focus on issues that fall outside the attention of the majority of employees or investors (King 2016). These types of campaigns have been used successfully in many different fields, including the ‘birth of the corporate campaign’ in workers unions (“ACTWU vs. J.P Stevens: 1976-1980” n.d.), fair trade (Harris 2021) and environmental protection (“Alaska Wilderness League vs. The Bush Administration: 2001-2002” n.d.).

These campaigns use a variety of tactics; from more cooperative approaches such as promoting change from within the company by supporting aligned stakeholders or offering technical assistance, to adversarial approaches such as media campaigns (Capriati 2018) or, in the case of labour unions, strikes. When cooperative approaches are used, this is better viewed as corporate outreach, although this is often the first stage of such campaigns when working with the most aligned companies within an industry. Whenever adversarial approaches are threatened, corporate campaigns can be viewed as a form of extortion where an interest group threatens a company with some action if they don’t capitulate to their demands.

Theories for explaining the success of these movements depend on the tactics employed by the interest groups. The most simplistic tactic is economic disruption caused by direct action. When this is used, the aim of campaign groups is to directly disrupt the operations of the business, in order to impose large enough costs so they regard the costs of resistance as outweighing the costs of conceding to the group demands (Luders 2006; Spar and La Mure 2003). These tactics are most commonly used by primary stakeholders, such as labour unions who can use strikes or work to rule tactics to disrupt business. However, other movements have and continue to use direct action in a similar vein by blocking or disrupting supply chains through sit-ins or lock-ons.

Many movements are able to achieve change through corporate campaigns without the use of mass disruption tactics (King 2016). Such campaigns typically target public facing companies that have increasingly emphasised the value of intangible resources, such as their reputation. Over the past few decades, firms have increased the monitoring and value of their reputations and caused reputation management to become a major focus of corporate public relations (King 2016). Thus, in as far as reputation is or is perceived to be connected with profit or market value, or valued intrinsically by management (Tim Bartley and Child 2007), interest groups can ‘name and shame’ corporations without disrupting the day-to-day business and still achieve their goals.

WHAT IS THE VALUE OF A FIRM'S REPUTATION?

Why is reputation valuable to a firm?

As many modern anti-corporate campaigns have shifted towards targeting a firm’s reputation, understanding the value of their reputation is important for understanding the degree to which this can motivate a firm.

Compared to the financial fundamentals of a firm's value, it is easy to see reputation as a nebulous and intangible asset beyond the scope of analysts’ models. However, it is widely observed that the valuation and performance of companies is only in part driven by easily measurable financial information, particularly in the short term, with the difference often being attributed to market ‘sentiment’ (Cole 2012).

Some efforts to measure a firm's reputation focus on one overall judgement of a company either across all groups or within groups of stakeholders. Other conceptions of a firm's reputation split reputation into two components; cognitive and affective (Raithel and Schwaiger 2015). The cognitive component encompasses judgements surrounding the firm’s competence and reliability, while the affective component captures ‘feelings’ towards a firm, such as emotional appeal, attractiveness, or social and environmental responsibility.

Positive reputations have a number of potential favourable consequences, including the ability to charge higher prices, attract better applicants, and improve access to capital (Fombrun and Shanley 1990; Raithel and Schwaiger 2015; Srivastava et al. 1997). These ultimately influence the company's revenues, margins, and the existence of a competitive advantage (Smith, Smith, and Wang 2010). Corporate reputation has been found to create positive abnormal stock returns in the long term, particularly for non-financial aspects which are less likely to be priced in (Raithel and Schwaiger 2015), as well as providing a protective effect against crises (Schnietz and Epstein 2005; Wei, Ouyang, and Chen 2017).

What is the market value of a firm's reputation?

Various researchers have attempted to develop methods to quantify the relative proportion of a company's market cap that is attributable to their reputation. Thus far, this has been motivated to create better predictive models of a company's value for investors, and to provide more objective measures for reputation management within firms. However, it should be possible to leverage the same information in corporate campaigns to actively work against the value of a company's reputation; both by targeting companies with valuations that are more dependent on their reputation, and if interest groups actively target the same measures that companies use when managing their public relations.

Cole (2012), of Reputation Dividend, developed one such model by using regression analysis on a wide set of potential explanatory variables for a company’s market capitalisation, covering financial information and analytics alongside survey data from the ‘Most Admired Companies’ studies published by Management Today in the UK and Fortune in the US (Cole 2012). This survey measures reputation through the ratings of companies on nine criteria, from investment value and quality of management and products to social responsibility and ability to attract talent by a large sample of executives, directors, and securities analysts (Belanger 2022). The average of these was considered the overall strength of a company's reputation for Cole’s model. This information was run through multiple iterations and refinements. Cole’s model suggests that company reputations accounted for close to 26% and 32% of the total market capitalisation of the S&P 500 and FTSE 250 respectively. The variation in reputation contribution is even higher between individual companies, with a high of almost 58% (Apple) to a low of –39% (Sears Holdings). Reputation Dividend provides these evaluations each year in both the US and UK.

Other efforts to evaluate the value of a corporate reputation have taken a more direct route by surveying global executives for their direct estimates of this figure (Shandwick 2020). As with Cole’s (2012) estimate, Shandwick’s (2020) varied widely depending on the country. The average estimate was 63% of a firm's market value, but this was as low as 47% in the UK and Hong Kong, and as high as 76% in Brazil. On an individual firm level, about two-thirds of executives attributed over half their company’s value to their reputation and a third over three-quarters of its value. These figures are much higher than the estimates produced by reputation analysis, suggesting that executives might overvalue their company’s reputation. However the definition of reputation used here was broader than Cole’s, with many executives including the quality of products and services as the main contributor to a company's reputation, which is likely to have a significant effect on its market value.

Still, even if a firm's reputation makes up a large portion of a company's value, this does not reveal a company's willingness to pay to improve its reputation or avoid the cost involved in an anti-corporate campaign. Each of these variables will only be able to influence stakeholder perceptions to a degree.

HOW MUCH DAMAGE CAN CORPORATE CAMPAIGNS DO TO A FIRM'S REPUTATION?

In principle, it should be possible to quantify more precisely the costs that NGO activism imposes on particular firms or industries (Spar and La Mure 2003). Does the share price of targeted firms decrease during campaigns and increase after commitments? Or can we measure the hypothesised effect of such campaigns on other outcomes, such as expense on the cost of recovery, lost revenue, talent acquisition, and the cost of capital for firms?

The existing evidence shows that public announcements or media attention towards poor labour practices (Rock 2003; T. Bartley and Child 2011), pollution (Hamilton 1995; Rao 1996; Rao and Brooke Hamilton 1996), sexual harassment (Bouzzine and Lueg 2022; Borelli-Kjaer, Schack, and Nielsson 2021) and employee discrimination (Rao and Brooke Hamilton 1996) can have a significant effect on the stock price of affiliated organisations. However, there are conflicting results, with some studies not finding significant effects (Tim Bartley and Child 2010) depending on the events included and time period analysed. Still, most published studies find that these effects can be quite large, with statistically significant short-term effects from the studies cited above ranging from -0.82% (Rock 2003) to -5.67% (Rao 1996).

In some instances, these effects can persist across larger time scales, with Rao finding strong abnormal effects six months after reports of a company's environmental pollution (Rao 1996). Pentland Analytics’ review of 125 of the largest crises between 2008 and 2018 found that companies lost 5% of expected market capitalisation in the following 12 months (Pretty 2018). It is interesting to note that there was a large divergence in the sample, with a split emerging relatively quickly, within a week, between companies that subsequently gained value and those that lost a much greater share. Regardless of the outcome on the companies’ valuation, price volatility increased for all firms, signalling a higher risk associated with the firm increasing the cost of capital.

The longest-term evaluation of the effects of revelations of unethical business practises comes from Long et al (2016) who examined the effect announcement of various ethical violations, including bribery/illegal payments, employee discrimination, environmental pollution, and insider trading over a much larger timescale of 5-20+ years. They still found significant effects after 5 years, with -0.0357% (p=0.025) lower average daily return of firms with an announcement of unethical behaviour compared to other firms in their industries (Long 2016). Although they found no significant effect for all time frames greater than five years, statistically significant effects that persist across such long time frames suggest such announcements represent real persistent damage to the company's value.

To give a sense of the loss in market capitalisation these figures can represent, we can expand on the short-term effect found from anti-sweatshop campaigns by Rock (2003). Here they found a statistically significant effect on market capitalisation from as high as $166.6 million for Target to $3.25 million for K-Mart, with an average loss in market capitalization of $69.9 million or 0.82% (Rock 2003). Interestingly, the inverse effect was then observed for good news when Reebok, a shoe retailer, agreed to phase out the use of sweatshop labour with an abnormal return of 1.65% or $19.35 million. The effect on company value found across the studies cited above is more consistent in percentage terms varying from ~1-5%, however for total market capitalisation, this can mean much greater losses for larger companies.

More broadly, there are numerous case studies of scandals or campaigns that seem to have even more significantly reduced the reputation, value, and revenue of companies over the longer term. These include Chipotle, which lost almost two-thirds of its market value from an E. coli scandal (Bowman 2017), Wells Fargo, which lost $29 billion (9.2%) of its market value after a scandal about their business practices (Glazer 2018), and SeaWorld, which lost 50% of its market value over two years after the documentary titled ‘Blackfish’ was released (Stokes and Atkins-Sayre 2018).

One weakness of a lot of these event analysis studies is that they only analyse the effect of such announcements on short-term (a few days to a week) stock price fluctuations. The studies that examine a longer time frame of a year or more give a better sense of the long-term damage such scandals or campaigns can cause. Isolating the truly long term effects of these campaigns or scandals becomes increasingly difficult as companies are likely to have responded to the damage to their reputation and stock returns with policy changes that counteract their effects. Still, even if very long-term shifts are not achieved, CEOs confronted with scandals of such magnitude will face compensation penalties or dismissal based on the short and medium-term effects (Crisp 2021).

Another problem with generalising from these studies is that they only select the most ‘notable’ examples of campaigns that received a lot of media attention, thus making researchers aware of their existence. This means that these findings are most relevant to the effect of a successful campaign rather than the average effect of all campaigns.

In the same vein, all of the firms examined are public facing and traded with established reputations, whereas many firms within animal agriculture are privately owned and have some of the worst reputations, such as slaughtering companies (Albersmeier and Spiller 2008). Additionally, the animal agriculture industry already has a very critical perception from a number of stakeholders (Luhmann and Theuvsen 2016). Thus, these findings will not necessarily include campaigns targeted at producers or other actors further down the supply chain. The food retail and grocery industry, particularly higher end brands that put much larger stock in their reputation, are more likely to experience the significant and lasting damage from association with unethical practices observed in the literature.

If we take these estimates at face value, successful campaigns or revelations of unethical behaviour can reduce the value of affected firms between 1-5% in at least the short to medium term. If we apply this general heuristic to the food and grocery retail industry with an evaluation of $750 billion in the US (Grand View Research 2022) and £205 billion in the UK (Bedford 2022), then successful campaigns should do between $7.5 to $37.5 billion worth of damage in the US and £2 to £10 billion worth of damage in the UK. If we compare this to the estimated $6 billion investment required to shift from cage to cage-free systems in the US (Wong 2017) which has widespread success with gaining commitments, this figure looks quite reasonable.

WHAT ARE FIRMS’ MOTIVATIONS FOR GENERAL CORPORATE SOCIAL RESPONSIBILITY?

A tacit assumption in the disruption and reputation model of a corporate campaign is that companies act as rational actors who seek the least costly solution acting in accordance with the rational choice theory of organisational decision making. However, there is broad agreement in the existing literature that rational choice models do not reflect the real-world reality of individual decision making. This does not discount these models entirely, with the typical economic reasoning being that any individual will perform in ways we can't predict, but collective behaviour should act more in line with the economic theory long term.

Some researchers have made efforts to move towards descriptive models of decision making for which all observed decision making could be described, but these efforts also seem to have failed (Dillon 1998). Instead, each organisation may act according to a number of decision-making models or motivations, or vary the tool used across time or between contexts. Therefore, when attempting to model and anticipate the decision making and behaviour of organisations, one should not weigh any given model too heavily without significant previous experience of the behaviour of the organisations and decision-makers involved. These models can improve our ability to predict an organisation’s behaviour, but should be accompanied with observations of their motivations for previous decisions.

In the context of a corporate campaign, it is not uncommon for organisations to comply with activists' demands even when it may not be in their best interest to do so (Spar and La Mure 2003). In such instances, management may have strong commitments to the goals expressed by their potential critics. Unfortunately, the motivations for compliance with corporate campaigns have not been directly studied. Instead we can look at the wider literature on the general motivations of firms for Corporate Social Responsibility (CSR) initiatives, of which animal welfare is considered a part.

Broadly, companies’ motivations for CSR activities can be split into intrinsic and extrinsic motivations. Extrinsic motivations for CSR hold that CSR is instrumental for the goals of the company in the long run. This includes corporate reputation and the financial benefits that can accrue from this (examined in previous sections). Intrinsic motivations, on the other hand, come from business cultures that are committed to certain business principles, including moral duties (Graafland and van de Ven 2006). The relative importance of each motivation within these categories varies between industries, based on industry characteristics, relevant stakeholders, and the structure of their supply chain. However, some broad factors emerge across industries and contexts, and these can be seen as universal motivations for CSR.

Zhang et al (2018) conducted a systematic review of the available literature to identify the drivers, motivations and barriers to CSR in the construction industry (Zhang, Oo, and Lim 2019). Through content analysis they identified three external drivers of CSR; policy pressure, market pressure, and innovation and technology. These act as external coercive forces that can ‘force’ a corporation to undertake CSR activities. Alongside this, the most common internal motivations reported by companies were financial benefits, reputation, and organisational culture, which encompasses intrinsic motivations. Unfortunately, barriers to implementation were far more diverse, suggesting that there are a wide variety of potential barriers that vary across contexts. However, none apart from lack of knowledge or awareness of CSR within the organisation were that common.

In the energy sector, Agudelo et al (2020) conducted a systematic review on the drivers that motivate energy companies to adopt CSR (Latapí Agudelo, Johannsdottir, and Davidsdottir 2020). Here, the main drivers they identified were stakeholder engagement and satisfaction, corporate culture, and reporting, which is the publication of CSR activities.

In the financial sector, Wu et al (2013) studied the motives of banks to engage in CSR in part to understand the varied relationship between CSR and financial performance (Wu and Shen 2013). They found that the main drivers were strategic instrumental reasons, altruism (conducting CSR for its own sake), and greenwashing, which attempts to enhance corporate image without significantly changing the business.

These same motivations have also been observed in decision makers in many other contexts, such as professional sports (Babiak and Trendafilova 2009) and in a wider sample of firms in developing economies (Ali, Wilson, and Husnain 2022).

Cross-industry studies have found some general trends among the motivation of firms depending on size. In a survey of 111 large and small Dutch firms, Graafland et al (2006) found that large firms were more confident about the financial payoff of CSR than smaller firms on average, as the reputational mechanism is more important to them and they tend to have a longer time horizon than other companies in their industry. However, this difference was quite small with all firms reporting high agreement with both moral and strategic motivation for CSR (Graafland and van de Ven 2006). It was also of note that there was a stronger correlation between moral motivations and CSR performance than the strategic view.

Although these larger-scale industry-wide reviews of CSR do provide us with the general motivations for CSR, given variation in industry characteristics the main barriers will differ across industries. Fortunately, there has been some research into the use of CSR in the food industry supply chain. As with other industries, the main drivers behind CSR are improved competitiveness, scrutinisation by stakeholders, reputation, and legitimacy (Luhmann and Theuvsen 2016; Heyder and Theuvsen 2012). However, compared to other industries there is a greater emphasis on the pressure from NGOs, with this being the most frequently mentioned motivation or concern driving CSR in agribusiness (Maloni and Brown 2006; Hartmann 2011). It is also frequently noted that this pressure is most likely to be targeted at larger firms, making them more likely to implement CSR practices.

The existing literature on motivation for firm CSR initiatives is frequently subject to numerous methodological problems. Most notably, low response rates skew the sample towards those more actively involved in CSR, and possible social desirability bias towards more moral and less financial motivations.

From the existing research on the drivers of CSR across all industries we see that consistent motivations are strategic, reputational, and moral. These findings align with theories surrounding the mechanisms for corporate campaigns through the strategic and reputational motivations. The final motivation, moral, can be observed in industry leaders who sometimes choose to implement CSR or improved welfare practices either before activists begin any outreach or during the corporate outreach stage before any threats of a public campaign. These companies then act as examples for others, showing that the improvements are possible, and they can lead the way for their peers through the process of institutional isomorphism (Frank den Hond 2007).

Thus we can see that to measure the motivation of different companies, and how much it is possible to push for, we must both understand the value of and damage a corporate campaign can do to a reputation as well as the intrinsic motivations of key decision makers. The extrinsic motivation in some sense acts as a lower bound to the investment a firm should be willing to pay to maintain its good standing amongst its stakeholders, while intrinsic moral motivations can increase this further for some firms. However, in this case it is important to note the general finding that pushing on extrinsic motivation tends to diminish intrinsic motivations for an action (Frey and Jegen 2001).

WHAT ARE THE MAIN FACTORS THAT AFFECT THE SUCCESS OF CORPORATE CAMPAIGNS?

The damage that revelations of unethical business practices or corporate campaigns can do is significant. However, there are other barriers that may prevent a firm from complying with the requests of activists.

Sheoin (2014) outlines various possible explanations for the failure of a number of previous corporate campaigns (Mac Sheoin 2014). Some of the reasons outlined that are behind the failure of previous campaigns revolve around mistakes or the tactics used. For example, during Greenpeace's campaign over the disposal of the offshore oil rig ‘Brent Spar’, a mistake in the estimation of the amount of toxic material on the rig was used to cast doubt on Greenpeace's scientific credentials. Another example is when the BBC interviewed an activist posing as a spokesperson for a company responsible for a chemical leak in India that killed more than 15,000 people, resulting in less favourable framing for the victims by the media.

Another factor that can affect the success of campaigns is the structure of the industry. Schurman (2004) argues that ‘industry structures confer particular strategic openings and closures on social movements and render firms and industries more or less vulnerable to social movement actions’ (Schurman 2004). These include broader structures of the whole industry, such as the level of competition in an industry. More competition incentivises companies to seek to enhance their market positions or maintain them by mimicking the capitulation of other firms. In a similar vein, industries in which brand name and/or reputation is important to competition should be more vulnerable to attack (Debora L. Spar 2008; Mac Sheoin 2014). These include industries with more concentrated pressure points in their commodity chain such as a small number of buyers, particularly if these buyers have weaker social and economic relationships with the suppliers. For example, if a country's retail market is dominated by four firms and the product targeted is only a minor motivation for consumers to shop at that retailer such as goats cheese. This allows them to dissociate from the primary target in response to a campaign, putting significant pressure on the target (Schurman 2004).

The product as a whole can make the industry more vulnerable to attacks, such as products with negative health effects, have a negative environmental impact, or widely offending people’s moral sensibilities. However, a broad protective element for an industry is if it offers significant economic, national security, or political benefits to a state (or ruling party), where it will then receive greater state protection against challengers (Schurman 2004).

Vulnerabilities can also occur at the company level, such as associations with stakeholders with poor reputations, or if a company has made public commitments around a cause or proclaims a value that it can be reasonably shown not to uphold (Schurman 2004).

Outside of industry-wide or firm-level considerations, as predicted by a model of companies as rational actors, we find that higher transactions push firms towards the path of resistance (Debora L. Spar 2008). This is typically evaluated from a financial cost perspective, but should also be considered from a logistical or knowledge perspective. With this being a commonly cited reason for barriers to general social responsibility (Zhang, Oo, and Lim 2019). This is common with corporate social responsibility, or more friendly campaigns where initial cooperation with the industry is to educate them on alternative business practices. Alternatively, if a practice is currently integral to the supply chain and alternatives are not easily available, then regardless of what it may theoretically cost to shift this will not be seen as possible for the industry. An example of this would be where chick culling was 10 years ago, when the technology was in development but no concrete examples or alternatives were available. A corporate campaign on a topic such as this would be futile.

Another element of the ask which has been shown to affect the likelihood that companies respond positively to interest groups requests is request legitimacy (Eesley and Lenox 2006). This can be defined as the degree to which the issue raised by a stakeholder group request is well accepted and well defined by the public. Thus simpler asks that are more understandable to the general public will generally elicit a positive response suggesting composite asks are more difficult to campaign for, with the possible exception of certifier-based campaigns such as the fair trade campaigns or Aquatic Animal Alliance’s certifier campaign.

Summary of beneficial factors:

High level of competition between firms in the targeted industry

Reputation is important to competition

Buyers have weaker social and economic relationships with the suppliers

The targeted product has negative health, environmental or moral consequences

Target companies have associations with stakeholders with poor reputations

The company proclaims a value that it can be reasonably shown not to uphold

The ask is well accepted and well defined by the public

Summary of disadvantages:

Product provides significant benefits to a state (or ruling party)

Higher costs for capitulation to demands

Logistical or knowledge barriers to implementation

METHODS FOR EVALUATING THE TRACTABILITY OF AN ASK?

Given the theoretical background of corporate campaigns and observations of barriers to companies' capitulation to demands, there are a few indicators or research methods we can use to assess the tractability of a corporate ask.

The first, as outlined above, is by constructing a theoretical rational choice model of the company's or industry's decisions. This compares the full economic cost of the choice to comply with an interest group's demands to the reputational and financial damage the group is able to achieve through an anti-corporate campaign (Baron and Diermeier 2007). This includes both capital investment and the effect of ongoing price changes on the profitability of an industry. Thus, this evaluation would include the full net present cost of shifting the industry to the improved practice. Additional elements for composite asks would be prioritised based on the cost-effectiveness of the improvement on welfare for the corporation, limiting for the number of elements determined by the expected damage a campaign could cause. Under this model more elements could be included if improvements were cheap and easy to implement or the industry is particularly vulnerable to anti corporate campaigns. With examples of when this might be the case outlined in previous sections such as industries with larger more reputational driven firms in tight competition with each other and without a strong dependence on the product being targeted.

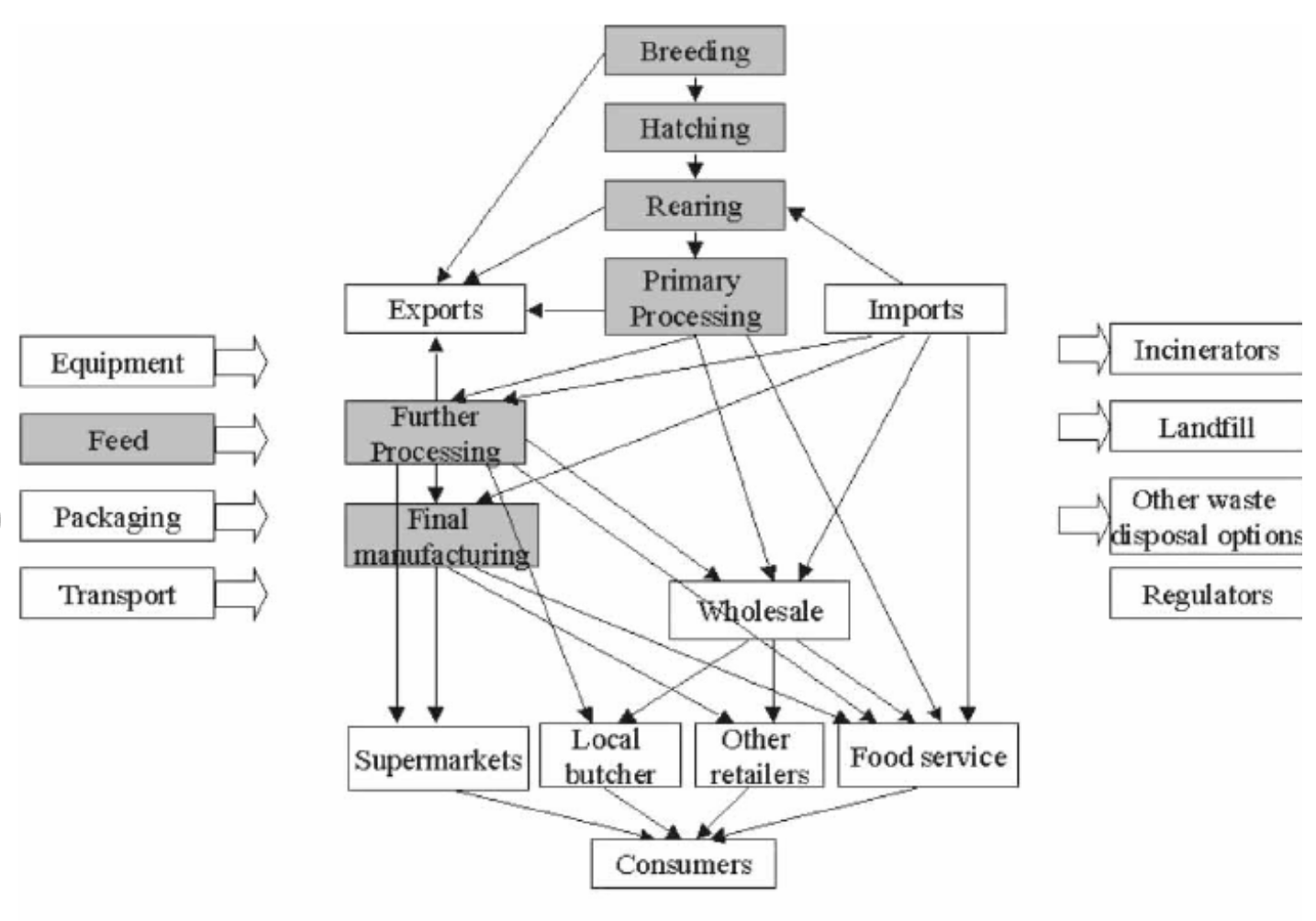

The next method is developing an understanding of the context of the campaign, including the stakeholders involved in the supply chain for the product as well as the power dynamics between each other and attitudes towards potential improvements. This would require multiple different research projects, beginning with a map of the supply chain for the product. For animal products this would include all life stages. An example of what such a map would look like is found below. This would highlight the key actors involved and the level of dependency of each stage on others further up or down the supply chain, identifying pressure points that would be weak to a corporate campaign.

Map of the chicken supply chain (Yakovleva et al. 2004)

When we have identified the key categories of companies present in the supply chain, the next project should be on creating a corporate profile of the likely targets for the campaign. This should include the number of individuals present in their supply chain, financial indicators, major stakeholders and the history of and pledges towards CSR and animal welfare. This, combined with profiles of key company executives, will identify companies that are more or less intrinsically motivated towards better animal welfare as well as which companies are weakest to anti-corporate campaigns.

The most difficult method for evaluating this is to directly survey target stakeholders or others in the supply chain about their willingness to adopt the practices and barriers or drivers for this. A good example of this is Sinclair et al (2019), who used focus group sessions with livestock industry leaders to discuss their willingness to embrace pre-slaughter stunning (Sinclair et al. 2019). Although in principle this could be achieved through a variety of methods including surveys, one-on-one interviews, or more intensively consensus methods for expert opinions such as the Delphi method (Hohmann, Cote, and Brand 2018). The main barrier to using this method will likely be the willingness of industry stakeholders to engage with activists in gathering the information.

CONCLUSION

As we can see from the available literature, corporate campaigns and scandals in relation to unethical business practices can cause significant and potentially long lasting damage to a firm's reputation and financial performance. Still additional research into the financial and reputation effects of historic animal advocacy corporate campaigns on retailers would help to ensure that these effects generalise to our specific context. From the existing research in related fields we observe that the damage to a firm depends on its size, existing reputation, and the efficacy of the campaign.

If firms' motivations for compliance with interest groups demands was entirely based on a rational economic calculus, this could be used to evaluate the degree of financial investment activities organisations could push for with their campaigns. However, this simplistic model of firm behaviour does not translate to observed motivations for CSR and responses to previous campaigns. It fails to account for the intrinsic motivations of some firms as well as non-financial factors such as logistical or knowledge barriers to implementation. As well as the basic observation that humans don’t act according to this ‘ideal’ rational economic calculus. Therefore, although such simplistic models are able to provide some insight into the magnitude of the ask that can be made, they need to be used alongside an understanding of the specific context of the campaign including the supply chain, key stakeholders and their motivations. As corporate campaigns are ultimately social phenomena, precise quantitative estimates are not reliable, but various research methods can be used to make more informed decisions on the magnitude of the ask that can be made.

BIBLIOGRAPHY

“ACTWU vs. J.P Stevens: 1976-1980.” n.d. Corporate Campaign, Inc. Accessed March 14, 2022. http://www.corporatecampaign.org/history_actwu_jp_stevens_1978.php.

“Alaska Wilderness League vs. The Bush Administration: 2001-2002.” n.d. Corporate Campaign, Inc. Accessed March 14, 2022.

http://www.corporatecampaign.org/history_alaska_bush_administration_2001.php.

Albersmeier, Friederike, and Achim Spiller. 2008. “Supply Chain Reputation in der Fleischwirtschaft.” 0811. Diskussionsbeitrag.

https://www.econstor.eu/handle/10419/29661.

Ali, Waris, Jeffrey Wilson, and Muhammad Husnain. 2022. “Determinants/Motivations of Corporate Social Responsibility Disclosure in Developing Economies: A Survey of the Extant Literature.” Sustainability: Science Practice and Policy 14 (6): 3474.

Babiak, Kathy, and Sylvia Trendafilova. 2009. “Corporate Social Responsibility in Professional Sport: Motives to Be ‘Green.’” Social Responsibility and Sustainability in Sports. Ediciones de La Universidad de Oviedo, Oviedo, Spain, 31–58.

Baron, David P., and Daniel Diermeier. 2007. “Strategic Activism and Nonmarket Strategy.” Journal of Economics & Management Strategy 16 (3): 599–634.

Bartley, T., and C. Child. 2011. “Movements, Markets and Fields: The Effects of Anti-Sweatshop Campaigns on U.s. Firms, 1993-2000.” Social Forces; a Scientific Medium of Social Study and Interpretation 90 (2): 425–51.

Bartley, Tim, and Curtis Child. 2007. “Shaming the Corporation: Globalization, Reputation, and the Dynamics of Anti-Corporate Movements.” In Annual Meeting of the American Sociological Association, New York. Available at Http://www. Allacademic. com/meta/p184737_index. html.(Accessed March 1, 2009.). Citeseer. http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.218.5885&rep=rep1&type=pdf.

———. 2010. “Shaming the Corporation: Social Movement Pressure and Corporate Social Responsibility.” Unpublished Manuscript. https://businessinnovation.berkeley.edu/wp-content/uploads/businessinnovation-archive/WilliamsonSeminar/bartley021810.pdf.

Bedford, Emma. 2022. “UK Grocery Market Value 2026.” Statista. 2022. https://www.statista.com/statistics/330171/grocery-retail-market-value-in-the-united-kingdom-uk/.

Belanger, Lydia. 2022. “Methodology for World’s Most Admired Companies (2022).” Fortune. February 2, 2022. https://fortune.com/franchise-list-page/methodology-worlds-most-admired-companies-2022/.

Borelli-Kjaer, Mads, Laurids Moehl Schack, and Ulf Nielsson. 2021. “#MeToo: Sexual Harassment and Company Value.” Journal of Corporate Finance. https://doi.org/10.1016/j.jcorpfin.2020.101875.

Bouzzine, Yassin Denis, and Rainer Lueg. 2022. “The Reputation Costs of Executive Misconduct Accusations: Evidence from The# MeToo Movement.” Scandinavian Journal of Management 38 (1): 101196.

Bowman, Jeremy. 2017. “Qdoba’s Sale Is Bad News for Chipotle.” The Motley Fool. December 1, 2017. https://www.fool.com/investing/2017/12/01/qdobas-sale-is-bad-news-for-chipotle.aspx.

Capriati, Marinella. 2018. “Cause Area Report: Corporate Campaigns for Animal Welfare.” Founders Pledge. https://founderspledge.com/research/fp-animal-welfare.

Cole, Simon. 2012. “The Impact of Reputation on Market Value.” World Economics-Abingdon 13 (3): 47–68.

Crisp. 2021. “Evaluating the Real Cost of a Brand Crisis.” Crisp (blog). July 22, 2021. https://www.crispthinking.com/blog/evaluating-the-real-cost-of-a-brand-crisis.

Debora L. Spar, Lane T. La Mure, ed. 2008. “The Power of Activism: Assessing the Impact of NGOs on Global Business.” In Ethical Dilemmas in Management, 93–116. Routledge.

Dillon, Stuart M. 1998. “Descriptive Decision Making: Comparing Theory with Practice.” In Proceedings of 33rd ORSNZ Conference, University of Auckland, New Zealand. https://www.orsnz.org.nz/conf33/papers/p61.pdf.

Eesley, Charles, and Michael J. Lenox. 2006. “Firm Responses to Secondary Stakeholder Action.” Strategic Management Journal 27 (8): 765–81.

Fombrun, Charles, and Mark Shanley. 1990. “What’s in a Name? Reputation Building and Corporate Strategy.” Academy of Management Journal 33 (2): 233–58.

Frank den Hond, Frank G. A. de Bakker. 2007. “Ideologically Motivated Activism: How Activist Groups Influence Corporate Social Change Activities.” AMRO 32 (3): 901–24.

Frey, Bruno S., and Reto Jegen. 2001. “Motivation Crowding Theory.” Journal of Economic Surveys 15 (5): 589–611.

Glazer, Emily. 2018. “Fed Rebuke Costs Wells Fargo About $29 Billion in Lost Market Value.” The Wall Street Journal, February 5, 2018. https://www.wsj.com/articles/fed-rebuke-costs-wells-fargo-about-27-billion-in-lost-market-value-1517858678.

Graafland, Johan, and Bert van de Ven. 2006. “Strategic and Moral Motivation for Corporate Social Responsibility.” Journal of Corporate Citizenship. https://doi.org/10.9774/gleaf.4700.2006.su.00012.

Grand View Research. 2022. “Food & Grocery Retail Market Size Report, 2022-2030.” https://www.grandviewresearch.com/industry-analysis/food-grocery-retail-market.

Hamilton, James T. 1995. “Pollution as News: Media and Stock Market Reactions to the Toxics Release Inventory Data.” Journal of Environmental Economics and Management 28 (1): 98–113.

Harris, Jamie. 2021. “Social Movement Lessons from the Fair Trade Movement.” https://www.sentienceinstitute.org/fair-trade.

Hartmann, Monika. 2011. “Corporate Social Responsibility in the Food Sector.” European Review of Agricultural Economics 38 (3): 297–324.

Heyder, Matthias, and Ludwig Theuvsen. 2012. “Determinants and Effects of Corporate Social Responsibility in German Agribusiness: A PLS Model.” Agribusiness 28 (4): 400–420.

Hohmann, Erik, Mark P. Cote, and Jefferson C. Brand. 2018. “Research Pearls: Expert Consensus Based Evidence Using the Delphi Method.” Arthroscopy: The Journal of Arthroscopic & Related Surgery: Official Publication of the Arthroscopy Association of North America and the International Arthroscopy Association 34 (12): 3278–82.

King, Brayden G. 2016. “Reputation, Risk, and Anti-Corporate Activism: How Social Movements Influence Corporate Outcomes.” The Consequences of Social Movements. https://doi.org/10.1017/cbo9781316337790.009.

Latapí Agudelo, Mauricio Andrés, Lára Johannsdottir, and Brynhildur Davidsdottir. 2020. “Drivers That Motivate Energy Companies to Be Responsible. A Systematic Literature Review of Corporate Social Responsibility in the Energy Sector.” Journal of Cleaner Production 247 (February): 119094.

Long, D. 2016. “UNETHICAL BUSINESS BEHAVIOR AND STOCK PERFORMANCE.” Academy of Accounting and Financial Studies Journal; Arden Volume. https://search.proquest.com/openview/80ec7e23346d2c55735e0abc88c472fe/1?pq-origsite=gscholar&cbl=29414.

Luders, Joseph. 2006. “The Economics of Movement Success: Business Responses to Civil Rights Mobilization.” The American Journal of Sociology 111 (4): 963–98.

Luhmann, Henrike, and Ludwig Theuvsen. 2016. “Corporate Social Responsibility in Agribusiness: Literature Review and Future Research Directions.” Journal of Agricultural & Environmental Ethics 29 (4): 673–96.

Mac Sheoin, Tomás. 2014. “Transnational Anti-Corporate Campaigns: Fail Often, Fail Better.” Social Justice 41 (1/2 (135-136)): 198–226.

Maloni, Michael J., and Michael E. Brown. 2006. “Corporate Social Responsibility in the Supply Chain: An Application in the Food Industry.” Journal of Business Ethics: JBE 68 (1): 35–52.

Philanthropy, Open. 2016. “The Humane League — Corporate Cage-Free Campaigns.” http://www.openphilanthropy.org/focus/us-policy/farm-animal-welfare/humane-league-corporate-cage-free-campaigns.

Pretty, Dr Deborah. 2018. “Reputation Risk in the Cyber Age, The Impact on Shareholder Value.” Pentland Analytics. https://www.aon.com/getmedia/2882e8b3-2aa0-4726-9efa-005af9176496/Aon-Pentland-Analytics-Reputation-Re#:~:text=Reputation%20risk%20events%20can%20result,%2C%2024%2Dhour%20news%20cycle.

Raithel, Sascha, and Manfred Schwaiger. 2015. “The Effects of Corporate Reputation Perceptions of the General Public on Shareholder Value.” Strategic Management Journal 36 (6): 945–56.

Rao, Spuma M. 1996. “The Effect of Published Reports of Environmental Pollution on Stock Prices.” Journal of Financial and Strategic Decisions 9 (1): 25–32.

Rao, Spuma M., and J. Brooke Hamilton. 1996. “The Effect of Published Reports of Unethical Conduct on Stock Prices.” Journal of Business Ethics: JBE 15 (12): 1321–30.

Rock, Michael. 2003. “Public Disclosure of the Sweatshop Practices of American Multinational Garment/shoe Makers/retailers: Impacts on Their Stock Prices.” Competition and Change 7 (1): 23–38.

Sarek, Karolina. 2019a. “35 Independent Pieces of Evidence for Why New Corporate Campaigns Might (or Might Not) Work - EA Forum.” 2019. https://forum.effectivealtruism.org/posts/JWcNfLAJCxMPZCdCu/35-independent-pieces-of-evidence-for-why-new-corporate.

———. 2019b. “Did Corporate Campaigns in the US Have Any Counterfactual Impact? A Quantitative Model - EA Forum.”

Schnietz, Karen E., and Marc J. Epstein. 2005. “Exploring the Financial Value of a Reputation for Corporate Social Responsibility During a Crisis.” Corporate Reputation Review 7 (4): 327–45.

Schurman, Rachel. 2004. “Fighting ‘frankenfoods’: Industry Opportunity Structures and the Efficacy of the Anti-Biotech Movement in Western Europe.” Social Problems 51 (2): 243–68.

Shandwick, Weber. 2020. “The State of Corporate Reputation in 2020: Everything Matters Now.” KRC Research. https://www.webershandwick.com/news/corporate-reputation-2020-everything-matters-now/.

Šimčikas, Saulius. 2019. “Corporate Campaigns Affect 9 to 120 Years of Chicken Life per Dollar Spent.” Rethink Priorities. August 9, 2019. https://rethinkpriorities.org/publications/corporate-campaigns-affect-9-to-120-years-of-chicken-life-per-dollar-spent.

Sinclair, Michelle, Zulkifli Idrus, Georgette Leah Burns, and Clive J. C. Phillips. 2019. “Livestock Stakeholder Willingness to Embrace Preslaughter Stunning in Key Asian Countries.” Animals : An Open Access Journal from MDPI 9 (5). https://doi.org/10.3390/ani9050224.

Smith, Katherine Taken, Murphy Smith, and Kun Wang. 2010. “Does Brand Management of Corporate Reputation Translate into Higher Market Value?” Journal of Strategic Marketing 18 (3): 201–21.

Spar, Debora L., and Lane T. La Mure. 2003. “The Power of Activism: Assessing the Impact of NGOs on Global Business.” California Management Review. https://doi.org/10.2307/41166177.

Srivastava, Rajendra K., Thomas H. McInish, Robert A. Wood, and Anthony J. Capraro. 1997. “Part IV: How Do Reputations Affect Corporate Performance?: The Value of Corporate Reputation: Evidence from the Equity Markets.” Corporate Reputation Review. https://doi.org/10.1057/palgrave.crr.1540018.

Stokes, Ashli Q., and Wendy Atkins-Sayre. 2018. “PETA, Rhetorical Fracture, and the Power of Digital Activism.” Public Relations Inquiry 7 (2): 149–70.

“The Better Chicken Commitment Policy.” n.d. Accessed May 24, 2022. https://betterchickencommitment.com/policy/.

Wei, Jiuchang, Zhe Ouyang, and Haipeng Allan Chen. 2017. “Well Known or Well Liked? The Effects of Corporate Reputation on Firm Value at the Onset of a Corporate Crisis.” Strategic Management Journal 38 (10): 2103–20.

Wong, Vanessa. 2017. “Egg Makers Are Freaked out by the Cage-Free Future.” CNBC. March 22: 2017.

Wu, Meng-Wen, and Chung-Hua Shen. 2013. “Corporate Social Responsibility in the Banking Industry: Motives and Financial Performance.” Journal of Banking & Finance 37 (9): 3529–47.

Yakovleva, Natalia, Andrew Flynn, Ken Green, Chris Foster, and Paul Dewick. 2004. “A Sustainability Perspective: Innovations in the Food System.” IJCAI: Proceedings of the Conference / Sponsored by the International Joint Conferences on Artificial Intelligence 4. https://www.researchgate.net/profile/Natalia-Yakovleva-2/publication/228891953_A_Sustainability_Perspective_innovations_in_the_food_system/links/0fcfd512530a80500b000000/A-Sustainability-Perspective-innovations-in-the-food-system.pdf.

Zhang, Qian, Bee Lan Oo, and Benson Teck Heng Lim. 2019. “Drivers, Motivations, and Barriers to the Implementation of Corporate Social Responsibility Practices by Construction Enterprises: A Review.” Journal of Cleaner Production. https://doi.org/10.1016/j.jclepro.2018.11.050.

People interested in animal welfare and this post might be interested in applying to the Executive Assistant role at Mercy for Animals, which is working to end industrial animal agriculture.

This is a test by the EA Forum Team to gauge interest in job ads relevant to posts - give us feedback here.

Thank you for this very interesting post!

I have been curios on how much affect corporates campaigns have on companies bottom line, and I wonder if there is a simple way to show companies that people care and that campaigns will do damage to their companies. Many companies are convinced, or says at least, that consumers just say they care, but their purchasing habits shows something entirely different (there are many reasons for that of course). I am not entirely convinced they belive that, but would like to know if there is an easy way to dismiss this idea.

So I wonder what do you think is a good way to:

Any input would be greatly apricated!