Summary:

I am looking for feedback on a new tool being released by Yield & Spread called the FI Purpose Planner*. This template is meant to help individuals explore how different life choices—such as changing careers, donating more, or adjusting spending—can impact their Financial Independence (FI) and CoastFI timelines. My goal is to provide a dynamic way to model potential scenarios, making it easier to visualize the long-term consequences of various decisions.

After receiving valuable feedback on the FI-lanthropy Calculator I previously released, I’m once again reaching out to this community for insights.

(*Note on access: For the next week, the link to the FI Purpose Planner will be a direct link to the tool, after which I will revert the link back to my website where you have to submit a form to get the planner. It will remain free.)

Rationale for creation of the tool:

Financial Independence (FI) offers a powerful framework for living intentionally, aligning one’s resources with personal and giving/impact-related goals. I believe that understanding our finances can improve our ability to make informed, meaningful choices. For example, knowing where you stand on the path to FI can guide decisions about donating more, switching careers, taking a sabbatical to work on high-impact projects, or even choosing to allocate resources toward personal goals like homeownership, having children, etc.

I believe that ensuring you have financial security when making large life choices makes it much easier to help others. Additionally, your finances may also shape the timing of how you make an impact.

About the tool:

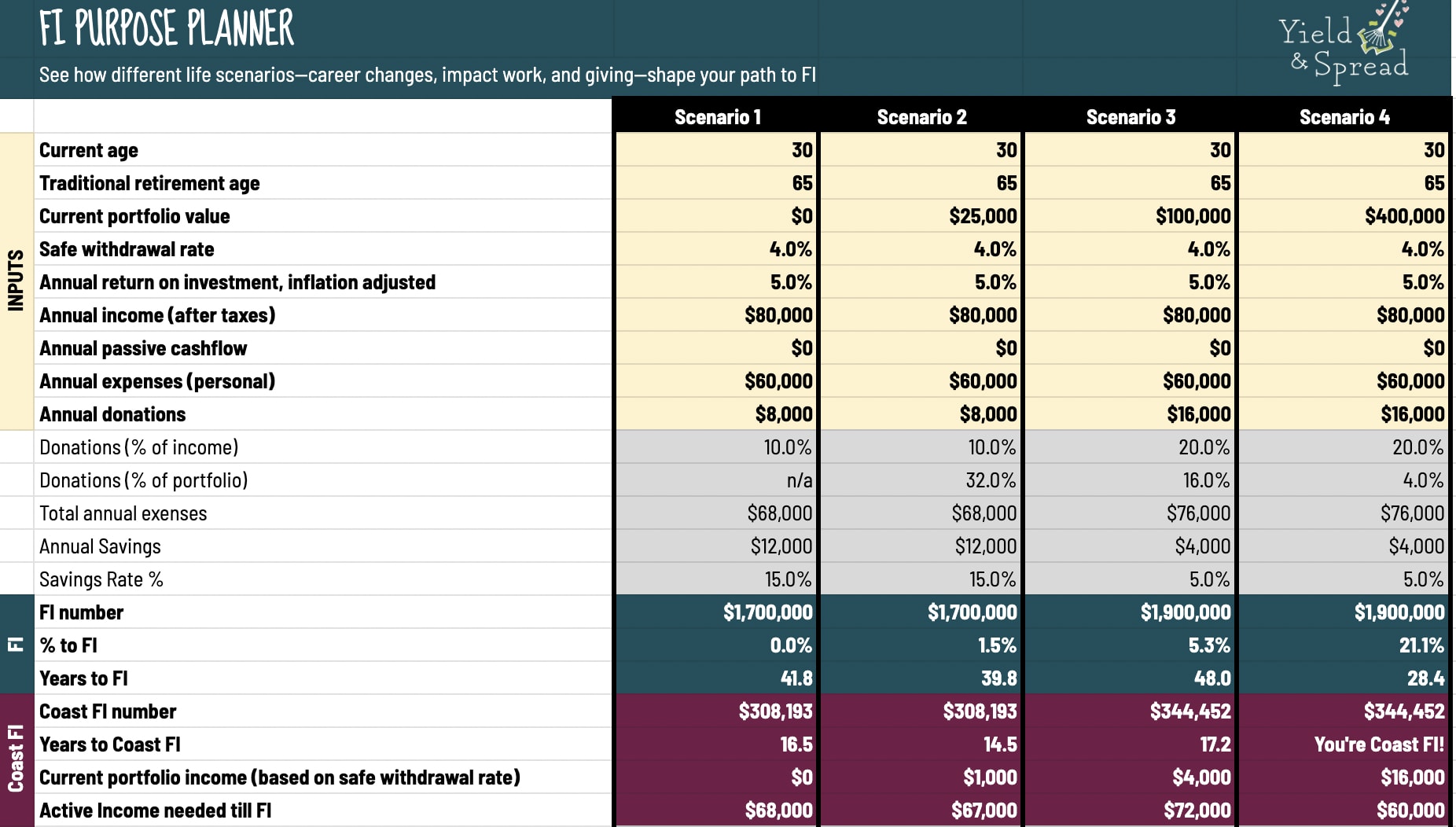

The FI Purpose Planner is designed to help individuals evaluate how various life choices affect their path to FI and CoastFI. It allows you to move beyond the standard "FI number" (typically 25x your annual expenses) by factoring in additional goals. The tool builds on the classic FI calculator by adding a more dynamic set of inputs to allow for greater flexibility.

Key features include:

- CoastFI output: This shows how far along you are on your path to CoastFI, as well as how much active income you'd need to maintain that status. I’ve discussed the concept of CoastFI in previous talks (namely at EAGx’s Virtual Conference last year), and I believe it provides a practical way to achieve your personal and professional goals faster.

- Projection of future portfolio at traditional retirement age: This shows what would happen if you continued working until traditional retirement age. I often find this information helps people realize they can take more risks and be willing to make change early because they may accumulate more wealth than needed otherwise.

- Donation Rate: A specific line item for those who plan to make regular donations as part of their financial plan. Making this input separate highlights the importance of this commitment.

I wanted the tool to be simple enough to understand and to be used independently without much guidance, but flexible enough that one can make it their own as needed. The spirit of the template is to help set you on the right path towards financial security...it's not meant for complex financial modeling, and you may very well need to do a more in-depth review of your finances with a professional to really pull the trigger on a big move. But this level of simplicity is often enough needed to get the ball rolling on a big life change, rather than spending hours and hours using more in-depth tools or outsourcing this work to a financial planner.

Example use cases:

I think offering real examples of how others have used this tool successfully is the best way to guide others as to how to use the planner:

- A computer programmer considering a move from a high-paying tech job to his dream role in the nonprofit sector was initially concerned about the significant pay cut. Using the FI Purpose Planner, he discovered he was already 80% of the way to Financial Independence. What once seemed like a huge financial sacrifice now felt like an empowered choice, giving him the confidence to pursue the career change.

- A philanthropically-minded individual wanted to take a progressive pledge—gradually increasing donations as his income or wealth grew—but was hesitant to go beyond 10% of his annual income. After experimenting with different pledge amounts in the planner, he realized he could comfortably increase his donation pledge to 20%, with the flexibility to explore further increases over time.

- A person new to Effective Altruism was considering the Giving What We Can pledge but didn’t think it was financially possible to do so. He had used many FI calculators before, but had never used one with a specific donation expense line item. The simple presence of having that as a separate input and being able to play around with donation rates supported him in taking the Giving What We Can pledge for the very first time.

- A married couple was debating a move to a new city but uncertain how the cost of living in each location would impact their financial security. By using the planner to map out housing costs, they were able to identify which cities would be the best fit for their budget and long-term goals.

- A young professional wanted to take some time off to travel but was concerned that she wouldn't be able to maintain her donations while on the path to FI. Using the FI Purpose Planner, she discovered that with a few adjustments to her savings rate, taking the year off wouldn’t derail her plans. In fact, she realized she was much closer to her financial goals than she had originally thought.

Tips for using the template effectively:

- Don’t use this tool to find your optimal life scenario. The goal here isn’t to find the perfect scenario – in fact, when we prioritize perfect finances we usually end up sacrificing important things in life. Instead, build out a number of scenarios. Ideally you have a best case scenario and a worst case scenario and see where you fall in the middle. Then this can act as a framework to ensure you are financially secure while exploring various options. Again it’s not about “getting it right”, it’s about pointing your compass in the right direction.

- Don’t be scared to play around with far-fetched ideas. Put in extreme variables. Increase your expected spending significantly. Change your income around. Work backwards towards a certain timeframe to FI. You might be surprised at the outputs.

- Do this in tandem with someone you trust. Getting an outsider’s point of view on your financial plans is extremely helpful. There may be life scenarios that you aren’t even thinking of yet. I often find having a third party to walk through this template leads to amazing conversations about the art of the possible.

Author background:

I am a member of both the FIRE and EA communities. I retired from my corporate real estate job 5 years ago at the age of 32. Now I live an early retiree lifestyle and also run an EA-aligned nonprofit Yield & Spread. We teach working adults how to learn and invest to build wealth, and we distribute all our profits after operating costs to effective charities. We have a lot of content around FI and giving, and this is another free tool we want to add to the roster.

I didn't read this piece fully or spend too long in the file, but passing on my feedback.

I found several parts unclear:

And I think a formula or two may be broken